Market Snapshot: Supreme Court Decision: Order in the Imports

The Supreme Court has ruled that tariffs imposed under the International Emergency Economic Powers Act (IEEPA) were unlawful, concluding that the executive branch exceeded its authority and encroached on Congress’s power of the purse. The decision marks a notable legal development in U.S. trade policy, though its economic implications may be more nuanced.

At issue is not only the legality of the tariffs themselves but also what happens next. While the ruling invalidates those IEEPA-based measures, the administration retains several alternative tools explicitly delegated to it by Congress to reimpose those duties in largely the same shape and form. Those tools include Section 122, Section 301, Section 232, and Section 338 authorities. In practical terms, this suggests that tariffs are unlikely to disappear but may instead be reconstituted under different legal tools.

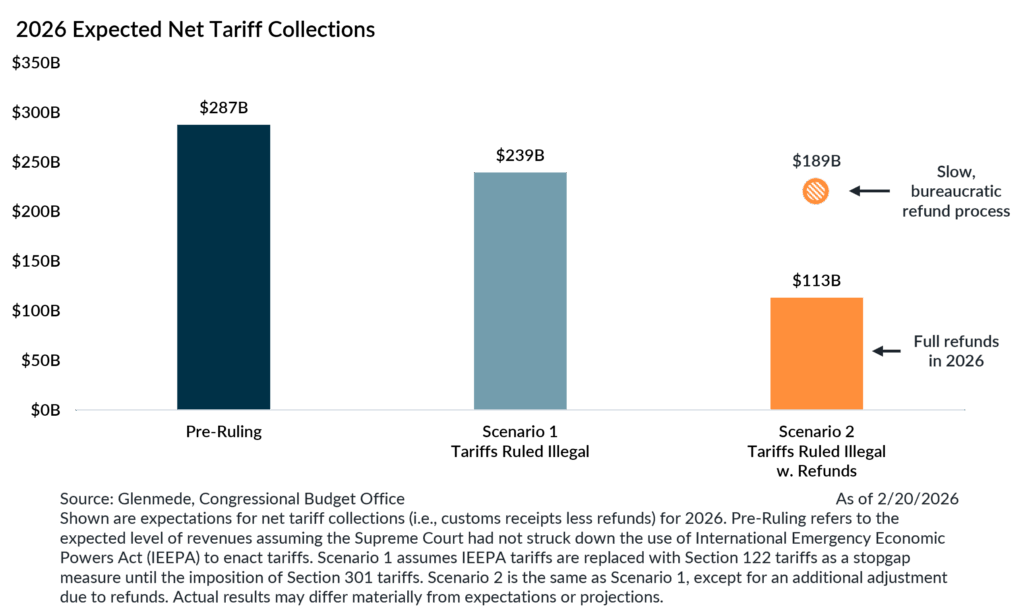

The near-term impact instead centers on timing and mechanics. Prior to the ruling, expected 2026 tariff collections were projected to approach roughly $290 billion. The path forward likely begins with swift imposition of Section 122 tariffs as a stopgap measure. They can be imposed immediately for up to 150 days, but the rates cannot exceed 15%. This could serve as a stopgap should the administration decide to proceed under Section 301, which requires it to initiate and conclude investigations to support longer-term actions. Under such a scenario, net collections may fall modestly short of prior expectation, to approximately $239 billion.

The larger swing factor is the treatment of refunds. If previously collected IEEPA tariffs were fully refunded this year, net tariff collections could fall materially to roughly $113 billion. However, a more plausible path involves a gradual, bureaucratic legal refund process extending into 2027, tempering the immediate fiscal impact. Using that gradual approach, net tariff collections this year may be closer to $190 billion.

From a macroeconomic perspective, the broader implication is that tariff policy may become less of a growth headwind in 2026 than it was in 2025. Even prior to the ruling, fiscal policy was poised to provide support through the scale of recently enacted legislation and an expected moderation in net trade drag. The Court’s decision potentially reinforces that trajectory by reducing net tariff collections and, in some scenarios, facilitating refunds that operate as a de facto fiscal injection.

Taken together, the net fiscal impulse for 2026 could approach the order of magnitude of 1% of GDP, depending on the pace and scope of replacement tariffs and refunds. That represents a meaningful shift relative to the prior year’s trade-related drag.

Near-term economic data may not immediately reflect this improvement. Businesses may respond to lower effective tariff rates by accelerating imports, a dynamic that subtracts from measured GDP through the net export channel. A similar pattern emerged in early 2025, when first-quarter growth was weighed down by import front-loading. Such effects tend to be temporary, reflecting timing rather than underlying domestic demand.

Legal uncertainty surrounding tariff authority remains, and administrative implementation details will matter. Still, the Supreme Court’s decision appears more likely to reshape the composition and timing of tariff collections than to fundamentally alter the direction of trade policy. The more durable takeaway is that the balance of fiscal forces in 2026 may lean more supportive of growth than previously assumed.

Jason Pride, CFA

Chief of Investment Strategy & Research, Glenmede

Michael Reynolds, CFA

Vice President, Investment Strategy, Glenmede

This material was produced by Glenmede Investment Management, LP or its affiliate The Glenmede Trust Company, N.A. (collectively, “Glenmede”) for informational purposes and is not intended as personalized investment advice to purchase, sell or hold any investment or pursue any particular strategy. Opinions and analysis expressed in this material are those of the author or investment team as of the date of preparation and may change without this document being updated. Views expressed do not necessarily reflect the opinions of all investment personnel at Glenmede and may not be reflected in all the strategies and products offered. Forecasts or estimates provided herein, including those related to market outlook are based on research including publicly available information, internally developed data and third-party sources believed to be reliable, but accuracy cannot be guaranteed. Future results may differ significantly depending on market, security specific, economic or political conditions. Charts and graphs provided herein are for illustrative purposes only. Past performance is no guarantee of future results. Indexes mentioned are unmanaged and do not include any expenses, fees or sales charges. It is not possible to invest directly in an index. Any index referred to herein is the intellectual property (including registered trademarks) of the applicable licensor. Any product based on an index is in no way sponsored, endorsed, sold or promoted by the applicable licensor and it shall not have any liability with respect thereto. Financial intermediaries are only permitted to distribute this material in accordance with applicable law and regulation. Such financial intermediaries are required to satisfy themselves that the information in this material is appropriate for any person to whom they provide it. Glenmede shall not be liable for the use or misuse of this material by any such financial intermediary.