Market Snapshot: The Minificent 7: Familiar Story, Different Index

Investors have become well acquainted with the Magnificent 7 and the outsized influence a small group of mega cap technology companies has exerted on large cap equity indices in recent years.2 Less appreciated is that a similar dynamic has quietly emerged in small caps.

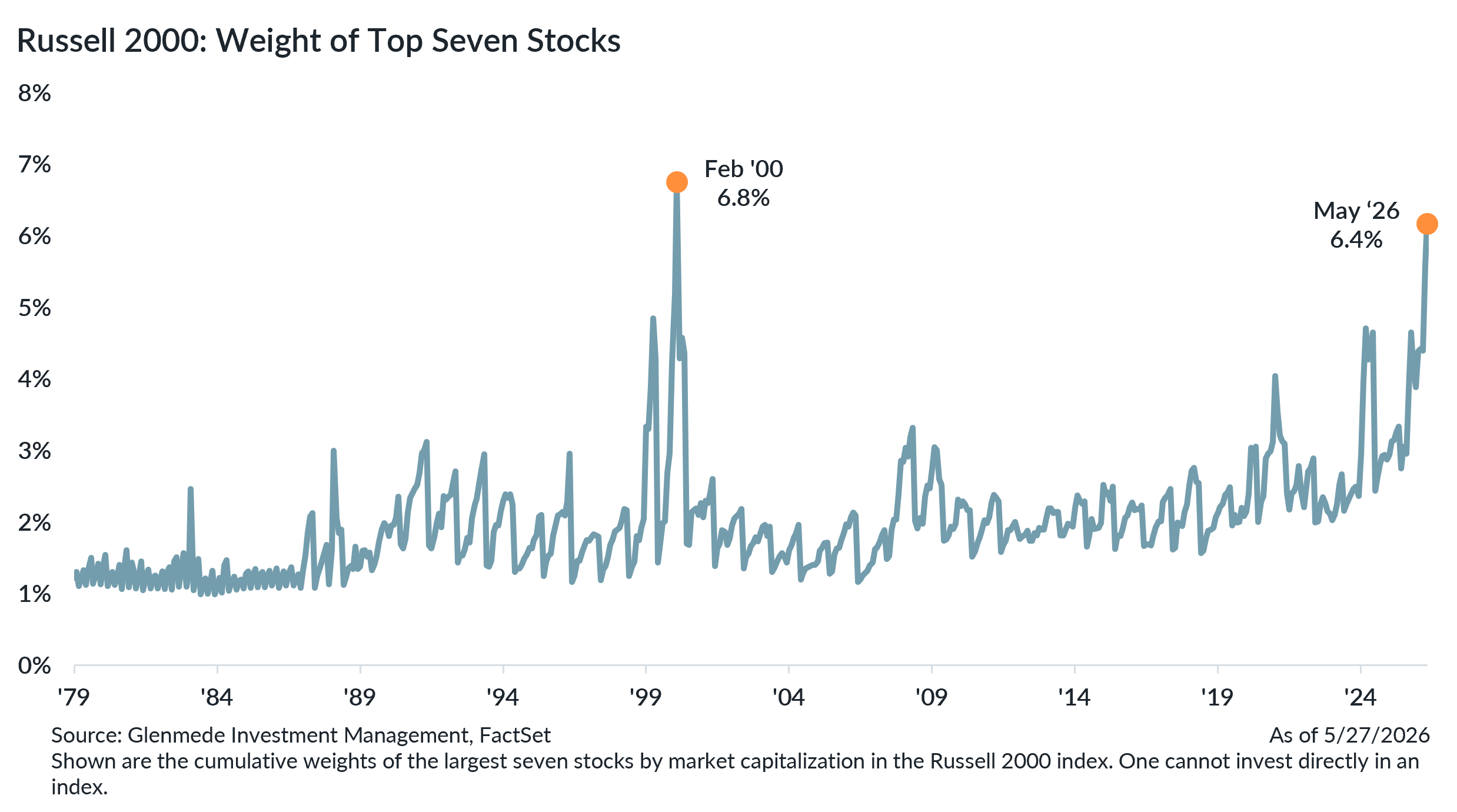

Today, the seven largest companies in the Russell 2000 account for roughly 6.4% of the index’s total weight, the second-highest concentration level recorded since 1979. The only higher reading occurred in February 2000, near the peak of the internet bubble.

That degree of concentration is particularly unusual in small caps. Structurally, the Russell 2000 tends to resist persistent concentration because successful companies often “graduate” into mid and large cap benchmarks as they grow. As a result, sustained dominance by a handful of names typically requires truly exceptional performance relative to peers in the short periods between index reconstitutions.

This year’s small cap leaders are a sort of “mini-Magnificent 7,” henceforth referred to as the “Minificent 7,” that share a notable common thread. While their business models differ, many are tied (either directly or indirectly) to the infrastructure buildout supporting artificial intelligence and next-generation computing demand:

- Bloom Energy: on-site and alternative power systems

- Credo Technology Group: high-speed connectivity and data transfer

- Sterling Infrastructure: physical infrastructure and site development

- IonQ: quantum computing and frontier technology

- Fabrinet: optical components and communications manufacturing

- NextPower: power infrastructure and grid-related exposure

- Coeur Mining: precious metals mining and production

Much like large cap’s Magnificent 7, the Minificent 7 reflects concentrated investor enthusiasm around a common technological and infrastructure theme rather than purely idiosyncratic company-specific developments.

Importantly, concentration within the Russell 2000 may also help explain why active management in small cap has faced an unusually difficult backdrop. Over the trailing one-year period ending in May, only 12% of managers in the Lipper Small Cap Core universe outperformed the Russell 2000 index. When leadership narrows dramatically, benchmark-relative performance can become increasingly dependent on owning a very small subset of rapidly appreciating stocks, many of which exceed typical position size limits for diversified active managers.

History suggests such environments can eventually reverse. In February 2000, when the Russell 2000’s concentration last reached comparable extremes, only 32% of small cap core managers had outperformed over the prior year. Yet in the subsequent twelve months, roughly 84% outperformed as market leadership broadened and speculative excesses faded.

No historical comparison is perfect, and today’s AI-driven investment cycle differs in important ways from the internet era. Demand tied to computing infrastructure, power availability, connectivity, and automation reflects genuine economic forces rather than purely speculative narratives. Still, the degree of concentration emerging within small caps is notable precisely because it is so historically unusual for the asset class.

The Russell index methodology itself may also play a role. Reconstitution frequency shifted from quarterly at launch, to semiannual in 1987, and then to annual in 1989. Beginning in 2026, the index will shift back to semiannual reconstitution. More frequent rebalancing may modestly reduce the persistence of concentration by allowing outsized winners to migrate more quickly into larger-cap benchmarks but may not address the multi-year trend toward higher concentration seen since 2019.

The emergence of the Minificent 7 illustrates that even small caps have not been immune to narrow market leadership. Yet history suggests that periods of extreme concentration can sow the seeds for a broader opportunity set ahead, particularly in an asset class where active management has historically thrived on dispersion and stock selection.

Val deVassal, CFA

Portfolio Manager, Disciplined Equity, Glenmede Investment Management

Alex Atanasiu, CFA

Portfolio Manager, Disciplined Equity, Glenmede Investment Management

1 Shown are the cumulative weights of the largest seven stocks by market capitalization in the Russell 2000 index. One cannot invest directly in an index.

2 The Magnificent 7 is composed of Nvidia, Apple, Microsoft, Amazon, Alphabet, Meta, and Tesla

This material was produced by Glenmede Investment Management, LP or its affiliate The Glenmede Trust Company, N.A. (collectively, “Glenmede”) for informational purposes and is not intended as personalized investment advice to purchase, sell or hold any investment or pursue any particular strategy. Opinions and analysis expressed in this material are those of the author or investment team as of the date of preparation and may change without this document being updated. Views expressed do not necessarily reflect the opinions of all investment personnel at Glenmede and may not be reflected in all the strategies and products offered. Forecasts or estimates provided herein, including those related to market outlook are based on research including publicly available information, internally developed data and third-party sources believed to be reliable, but accuracy cannot be guaranteed. Future results may differ significantly depending on market, security specific, economic or political conditions. Charts and graphs provided herein are for illustrative purposes only. Past performance is no guarantee of future results. Indexes mentioned are unmanaged and do not include any expenses, fees or sales charges. It is not possible to invest directly in an index. Any index referred to herein is the intellectual property (including registered trademarks) of the applicable licensor. Any product based on an index is in no way sponsored, endorsed, sold or promoted by the applicable licensor and it shall not have any liability with respect thereto. Financial intermediaries are only permitted to distribute this material in accordance with applicable law and regulation. Such financial intermediaries are required to satisfy themselves that the information in this material is appropriate for any person to whom they provide it. Glenmede shall not be liable for the use or misuse of this material by any such financial intermediary.