The Quarterly Recap Q2 2026: Economic & Market Recap

Executive Summary

- Geopolitical tensions pushed inflation higher, though a late‐quarter U.S.–Iran agreement helped ease some market concerns, while fiscal stimulus from tax and tariff refunds helped cushion the impact for households and businesses.

- The Federal Reserve held rates steady under new Chair Kevin Warsh, though a more hawkish set of projections and the introduction of five Fed task forces pointed to broader institutional change ahead.

- Equity markets rebounded sharply from a conflict‐driven drawdown to reach new highs, buoyed by robust first-quarter earnings; leadership continued to broaden benefiting smaller companies and international markets.

- The outlook for above‐trend growth remains intact, with potential key drivers of change in the second half of the year including mega IPOs, AI investment, new Fed leadership, and midterm elections.

Geopolitical Tensions and Inflationary Pressures

Geopolitical developments remained a key driver of markets and the economy in the quarter, as the conflict in Iran continued to reverberate through global energy markets, feeding quickly into energy-sensitive components of inflation. The Consumer Price Index rose 4.2% year-over-year in May, its highest reading since April 2023, while core inflation, which excludes food and energy, remained relatively well-anchored. This suggested the energy shock had yet to result in broad-based price pressures taking hold across the economy. The labor market also stabilized over the course of the quarter, showing signs of resilience with solid payroll growth and an unemployment rate that remained largely unchanged.

A U.S.–Iran agreement prompted a pullback in oil prices as markets began to price in a lower geopolitical risk premium. The agreement was best understood as a memorandum of understanding rather than a finished deal, as several of the thornier issues, including Iran’s nuclear program, had yet to be fully resolved. One of its more consequential provisions allowed commercial traffic to resume through the Strait of Hormuz, a critical transit route for energy commodities. While the number of vessels traversing the Strait began to normalize, traffic remained well below pre-conflict levels amid still-elevated geopolitical risks.

Against this backdrop, fiscal policy provided an offsetting tailwind. Consumers experienced the effects of the One Big Beautiful Bill Act (OBBBA), as retroactive income tax relief provisions resulted in larger-than-normal refunds and higher after-tax income for households. Businesses received separate relief through tariff refunds following the first-quarter Supreme Court ruling that duties collected under the International Emergency Economic Powers Act were unlawful. The administration moved to reimpose tariffs through alternative legal authorities: Section 122 tariffs came first, which allow emergency duties for balance of payments reasons; Section 301 tariff investigations on unfair trade practices remained in the works. Taken together, conditions pointed to an economy that remained on stable footing, as fiscal support helped cushion the drag from higher energy costs.

Warsh Takes the Helm at the Fed

The second quarter brought a change in leadership to the Federal Reserve, as Kevin Warsh took the helm as Chair. Warsh presided over his first meeting of the Federal Open Market Committee in June, at which policymakers kept rates unchanged, though updated projections revealed a more hawkish tilt. A conflict-driven rise in prices led roughly half of respondents to pencil in at least one rate hike before the end of 2026, a notable shift from prior expectations. Market-based pricing similarly converged on the prospect of one hike by year-end.

Warsh signaled a broader intent to reshape how the Fed operates beyond the rate decision itself. The June meeting featured a noticeably shorter policy statement, removing forward guidance. Warsh also introduced a series of task forces to review key functions of the central bank, including communications, the size of its balance sheet, its inflation framework, the data it relies on, and the interplay between productivity and the labor market. Taken together, these early moves suggest that further changes at the Fed are likely in the quarters ahead. The quarter closed with a Supreme Court ruling blocking the administration from removing Fed Governor Lisa Cook while litigation proceeds, affirming the constitutional basis for the Fed’s for-cause removal protections and its statutory independence.

Markets Stage a Historic Rally

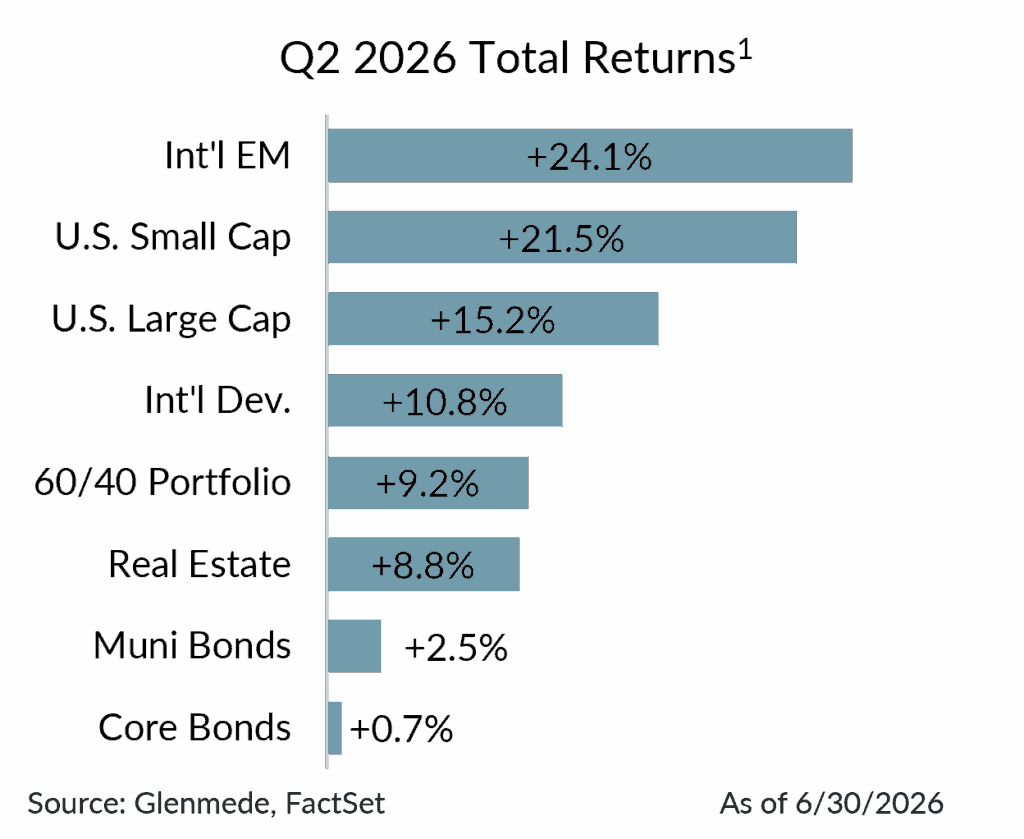

Equity markets staged a powerful rally in the second quarter, rebounding sharply from the geopolitical driven drawdown that had briefly erased the year’s gains. The S&P 500 climbed roughly 15%, reclaiming its prior highs and reaching new records. A strong earnings season underpinned the advance, with first quarter S&P 500 earnings growing 28% year-over-year, well above the 12% expected at the start of reporting season. Excluding non-recurring items, such as unrealized AI investment gains and tariff refunds, underlying growth was closer to 18%, still a solid result. Market leadership continued to broaden. Emerging markets surged 24%, driven in part by South Korea and Taiwan, which benefited from investor enthusiasm for AI-related opportunities outside the U.S. Domestically, small caps were also a standout, gaining more than 21% as improving earnings and more reasonable valuations drew investors beyond the largest stocks. Gold and bitcoin retreated, each falling about 14%.

In fixed income markets, yields traced a wide arc before partly round-tripping. The yield on 10-year U.S. Treasury bonds swung from roughly 4% in late February to nearly 4.75% in early May on energy-related supply disruptions, then fell back as inflation expectations eased following the U.S.–Iran deal. Core bonds finished the quarter in modestly positive territory, joining nearly every major asset class in the green.

Mid-Year Assessment: The Next Drivers of Change

The outlook for above-trend economic growth remains intact heading into the second half of the year. Glenmede expects U.S. GDP growth of approximately 2.7% in 2026, as fiscal stimulus from the OBBBA and early AI-driven productivity gains offset the drag from tariffs, higher energy prices, and slower job growth. While higher energy prices may weigh on growth, recession risk remains low given the economy’s increased energy independence, particularly should tensions ease.

Four developments stand to define the second half, the first of which is a wave of high-profile initial public offerings (IPOs). Total capital raised through public equity issuance could reach a record $200B+ this year, driven by a handful of mega cap listings rather than a broad surge in new issuance. SpaceX has already completed the largest IPO on record, with Anthropic and OpenAI both anticipated to follow in 2026 or 2027. Their near-term footprints in major indexes are likely to be modest given low initial share floats, though their weights are expected to increase as lockups expire and shares reach the market.

A second defining force is the scale of the bet on artificial intelligence, where capital spending by the major hyperscalers is approaching 2.5% of GDP, a magnitude that rivals the historic buildouts of the railroad and interstate highway systems. That spending stands as one of the year’s defining economic forces, even as the ultimate scale of AI’s productivity impact remains an open question. Rounding out the list are a Federal Reserve under new leadership navigating inflation that remains above target, and midterm elections that could reshape the policy landscape.

Premium equity valuations temper an otherwise constructive growth backdrop, though dispersion across regions and styles continues to leave pockets of relative value, particularly in small cap and international equities. Fixed income offers fairly priced yields and should continue to serve as a stabilizing force in portfolios.

1 Asset classes are represented by the following: Large Cap (S&P 500), Small Cap (Russell 2000), Int’l Dev. (MSCI EAFE), Int’l EM (MSCI EM), Real Estate (FTSE EPRA/NAREIT Developed), Core Bonds (Bloomberg U.S. Aggregate), Muni Bonds (Bloomberg Municipal), 60/40 Portfolio (60% MSCI ACWI, 40% Bloomberg U.S. Aggregate). Past performance may not be indicative of future results. One cannot invest directly in an index.

This material was produced by Glenmede Investment Management, LP or its affiliate The Glenmede Trust Company, N.A. (collectively, “Glenmede”) for informational purposes and is not intended as personalized investment advice to purchase, sell or hold any investment or pursue any particular strategy. Opinions and analysis expressed in this material are those of the author or investment team as of the date of preparation and may change without this document being updated. Views expressed do not necessarily reflect the opinions of all investment personnel at Glenmede and may not be reflected in all the strategies and products offered. Forecasts or estimates provided herein, including those related to market outlook are based on research including publicly available information, internally developed data and third-party sources believed to be reliable, but accuracy cannot be guaranteed. Future results may differ significantly depending on market, security specific, economic or political conditions. Charts and graphs provided herein are for illustrative purposes only. Past performance is no guarantee of future results. Indexes mentioned are unmanaged and do not include any expenses, fees or sales charges. It is not possible to invest directly in an index. Any index referred to herein is the intellectual property (including registered trademarks) of the applicable licensor. Any product based on an index is in no way sponsored, endorsed, sold or promoted by the applicable licensor and it shall not have any liability with respect thereto. Financial intermediaries are only permitted to distribute this material in accordance with applicable law and regulation. Such financial intermediaries are required to satisfy themselves that the information in this material is appropriate for any person to whom they provide it. Glenmede shall not be liable for the use or misuse of this material by any such financial intermediary.