Thought Leadership

Insights

April 01, 2026

Insights

April 01, 2026

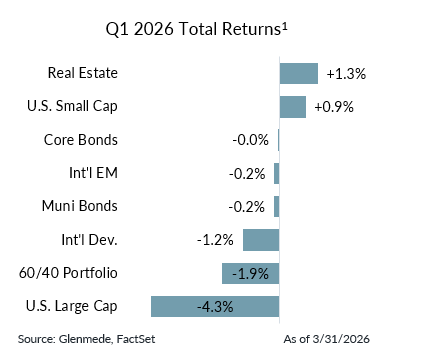

Executive Summary: Geopolitical tensions, particularly the escalation in Iran, introduced a new source of uncertainty, though economic data remained broadly constructive with some modest signs of softening …

News

March 16, 2026

News

March 16, 2026

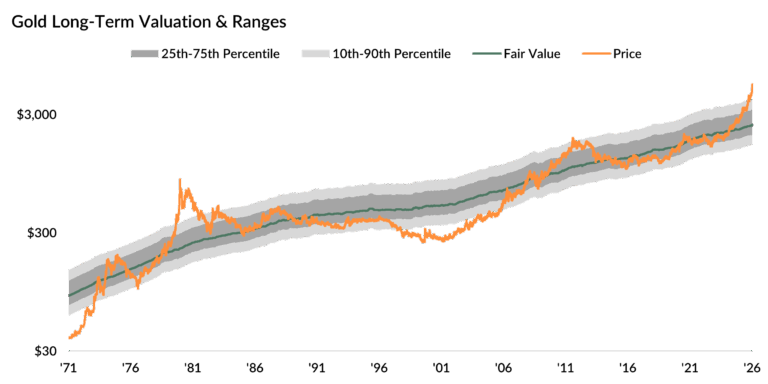

Gold has long maintained a distinctive role in diversified portfolios. Historically, it has functioned as a form of “insurance” by serving as a store of value, offering …

Insights

March 02, 2026

Insights

March 02, 2026

Over the weekend, negotiations between the U.S. and Iran evolved into a broader Middle Eastern military conflict. News reports state that coordinated U.S. and Israeli military operations …

News

February 20, 2026

News

February 20, 2026

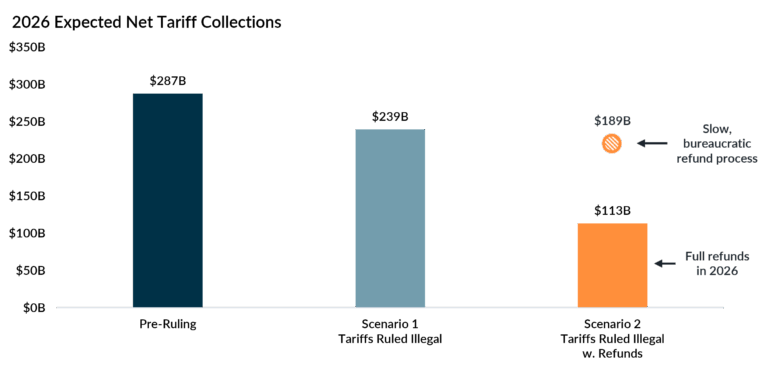

The Supreme Court has ruled that tariffs imposed under the International Emergency Economic Powers Act (IEEPA) were unlawful, concluding that the executive branch exceeded its authority and …

Insights

February 03, 2026

Insights

February 03, 2026

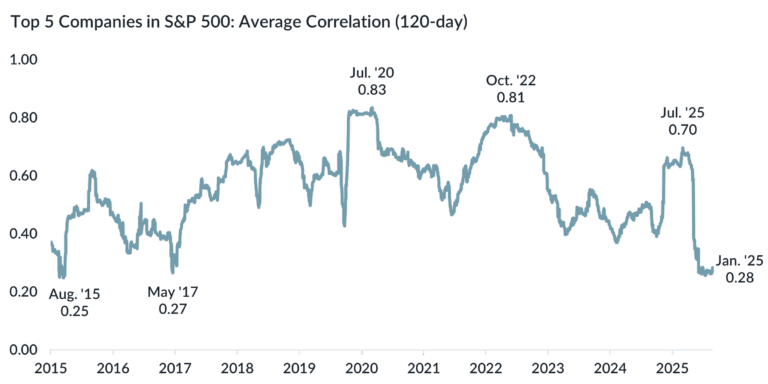

For much of the past decade, leadership among the largest stocks in the S&P 500 has been defined not only by outsized returns, but also by remarkable …

Insights

January 05, 2026

Insights

January 05, 2026

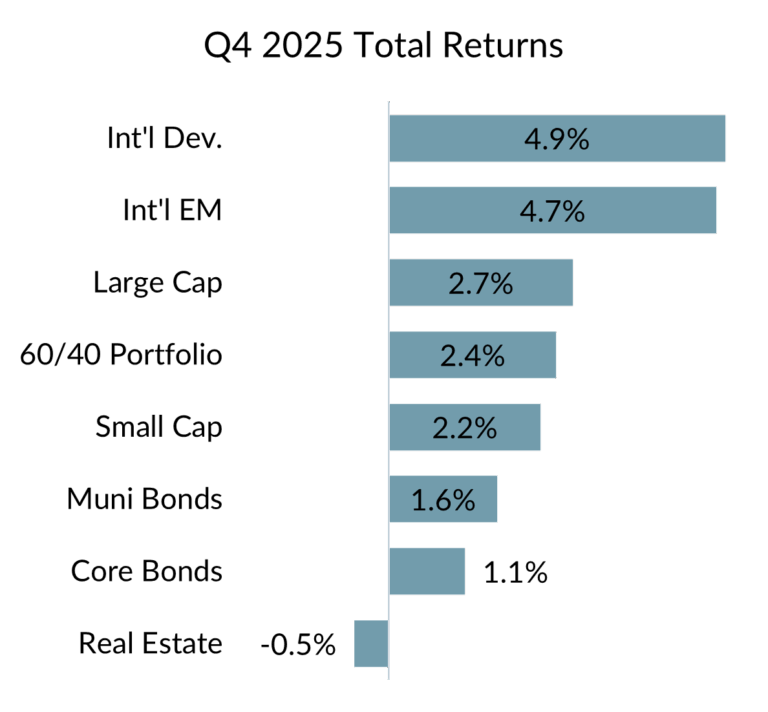

Executive Summary: The U.S. economy showed signs of continued resilience, even as government data disruptions and lingering policy uncertainty limited confidence in major economic indicators. As Congress …

Insights

November 19, 2025

Insights

November 19, 2025

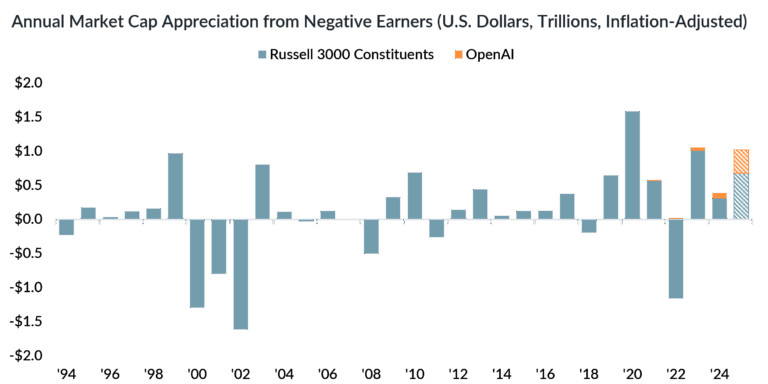

Negative-earning companies in the Russell 3000 have contributed meaningfully to total market cap gains in five of the last six full calendar years. If the first 10 …

Insights

November 05, 2025

Insights

November 05, 2025

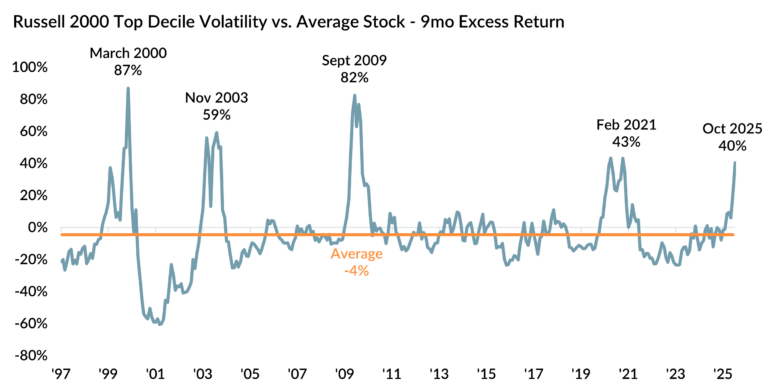

Ever since the calendar flipped to the second half of 2025, small caps have performed well relative to their larger counterparts. The Russell 2000’s 14.7% total return …

News

November 04, 2025

News

November 04, 2025

The actively managed equity portfolio offers investors access to today’s energy transition landscape PHILADELPHIA, November 4, 2025 — Glenmede Investment Management (GIM), an independently owned boutique asset …

Insights

October 20, 2025

Insights

October 20, 2025

Energy demand is rising, driven by artificial intelligence, electrification, and industrial reshoring, which are raising supply-demand imbalance and price risk. Past energy demand shifts were triggered by …