Extraordinary Earnings Until Proven Ordinary

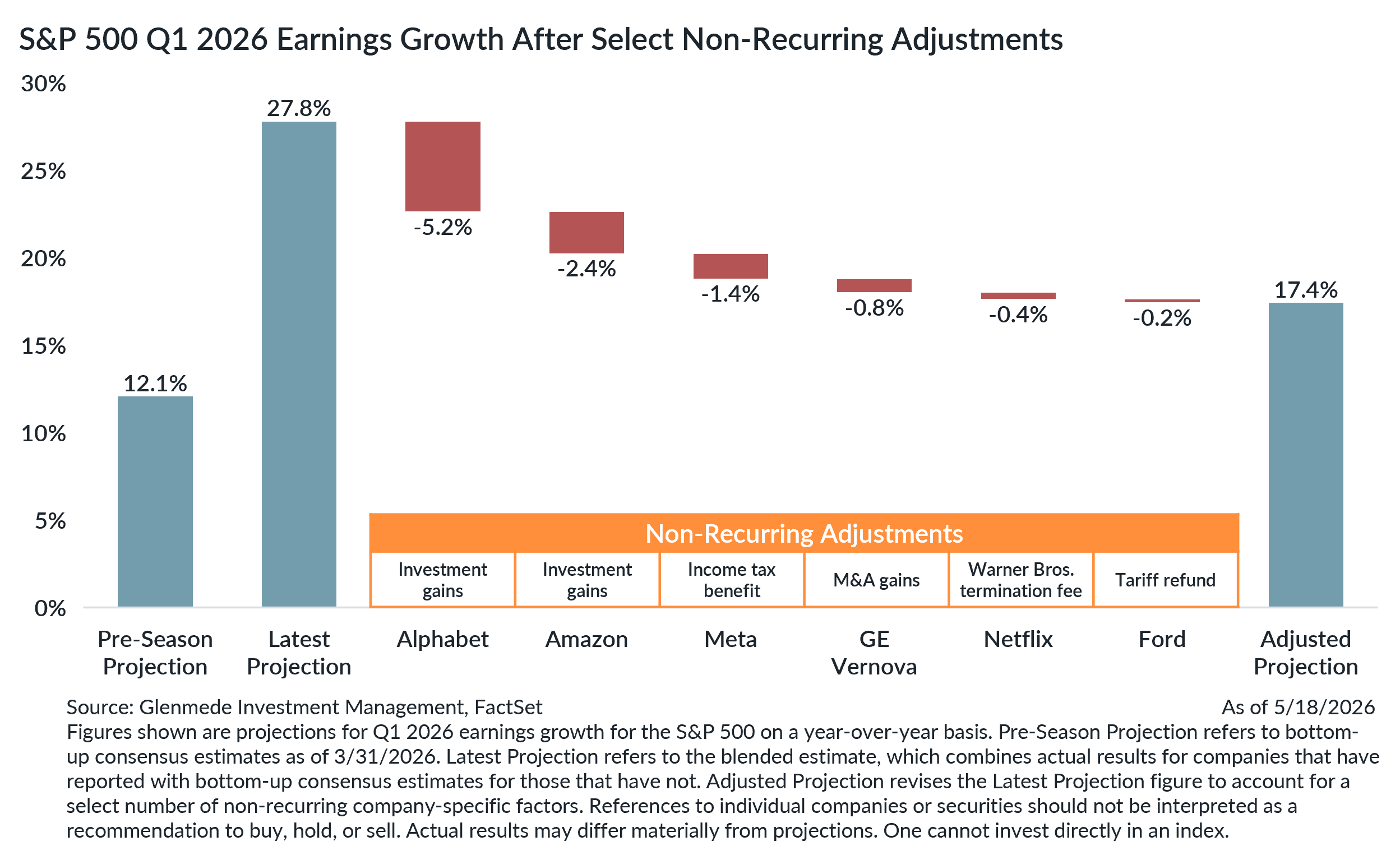

By almost any reasonable measure, the first quarter earnings season has been exceptionally strong. Entering reporting season, consensus expectations called for low double-digit earnings growth for the S&P 500 year-over-year. Instead, results are now tracking closer to 28%, representing one of the largest positive revisions in recent years. Roughly 84% of companies have exceeded expectations, with strength extending across multiple sectors and industries.

By almost any reasonable measure, the first quarter earnings season has been exceptionally strong. Entering reporting season, consensus expectations called for low double-digit earnings growth for the S&P 500 year-over-year. Instead, results are now tracking closer to 28%, representing one of the largest positive revisions in recent years. Roughly 84% of companies have exceeded expectations, with strength extending across multiple sectors and industries.

Importantly, the underlying earnings backdrop remains constructive. Demand tied to artificial intelligence infrastructure, cloud computing, and other digital investment continues to support strong revenue growth across large portions of the technology ecosystem. Capital spending trends tied to AI development remain robust, and those dynamics have helped reinforce the relative market leadership observed across those businesses involved in the buildout of data centers and compute capacity.

At the same time, a closer look beneath the surface suggests the headline earnings growth figures may somewhat overstate the strength of recurring operating fundamentals.

Several of the largest contributors to the quarter’s upside were driven by unusually large non-recurring items. Alphabet benefited from nearly $37 billion in unrealized gains tied to non-marketable equity securities. Amazon recorded substantial investment gains associated with Anthropic. Meta recognized a significant retroactive income tax benefit after the Department of Treasury clarified some details on the interplay between the corporate alternative minimum tax and previously capitalized R&D costs. GE Vernova reported a sizable M&A-related gain and Netflix benefited from a $2.8 billion termination fee related to its Warner Bros. agreement. Ford highlighted tariff-related refunds following the Supreme Court’s recent ruling on tariffs enacted under emergency powers.

Collectively, these items materially boosted reported earnings growth. Adjusting for these select non-recurring factors reduces the current S&P 500 earnings growth estimate from roughly 28% to closer to 17%. That remains a strong result, still comfortably above pre-season expectations, but presents a more balanced picture of underlying corporate profitability.

Importantly, the adjusted figures also reveal a broader earnings contribution outside of the largest mega cap companies. While technology and AI-related themes continue to dominate revisions and investor attention, the earnings season itself has been less concentrated than many of the figures initially suggested.

This distinction matters because markets often respond differently to recurring earnings power than to one-time accounting or investment-related gains. Extraordinary items can meaningfully affect near-term growth rates, but they may offer less information about the sustainability of future earnings trends.

Even after adjusting for these one-offs, the broader message from earnings season remains constructive. Corporate fundamentals continue to show resilience, AI-related investment remains a meaningful growth driver, and earnings growth has exceeded expectations by a healthy margin. However, the path from “strong” to “extraordinary” appears to have relied more heavily on non-recurring tailwinds than the headline numbers alone would imply.

John Kichula, CFA

Portfolio Manager, U.S. Large Cap Equity, Glenmede Investment Management

Mark Livingston, CFA

Portfolio Manager, U.S. Large Cap Equity, Glenmede Investment Management