Market Snapshot: A Semi-Concentrated Growth Index

The 2026 Russell Index reconstitution in late June will be a notable event for the Russell 1000 Growth Index, resulting in an unprecedented level of concentration in the information technology and communication services sectors. Post-reconstitution, the combined weight of these two sectors is expected to exceed 70% of the index, surpassing the prior peak reached in the first half of 2000.

The reconstitution of the Russell 1000 Growth Index should also reflect a significant reallocation within the technology sector. Software and hardware stocks are expected to see their weights decline by roughly 4.4% and 2.2%, respectively, while semiconductors are expected to gain a striking 8.7% share of the index. Those shifts reflect a trend that has been building beneath the surface: semiconductor performance has increasingly decoupled from other segments of the technology sector.

The artificial intelligence (AI) narrative has permeated markets broadly during the current bull cycle, but its impact has been especially pronounced within technology. This year’s “SaaSpocalypse” has weighed on some of the largest and most established software companies, as investors reassessed the potential for AI to disrupt or internalize traditional enterprise software models. Semiconductor stocks, by contrast, have remained at the center of the AI trade and have rallied to new highs. Year to date, 10 of the 16 semiconductor constituents in the Russell 1000 Growth Index have produced total returns exceeding 100%.

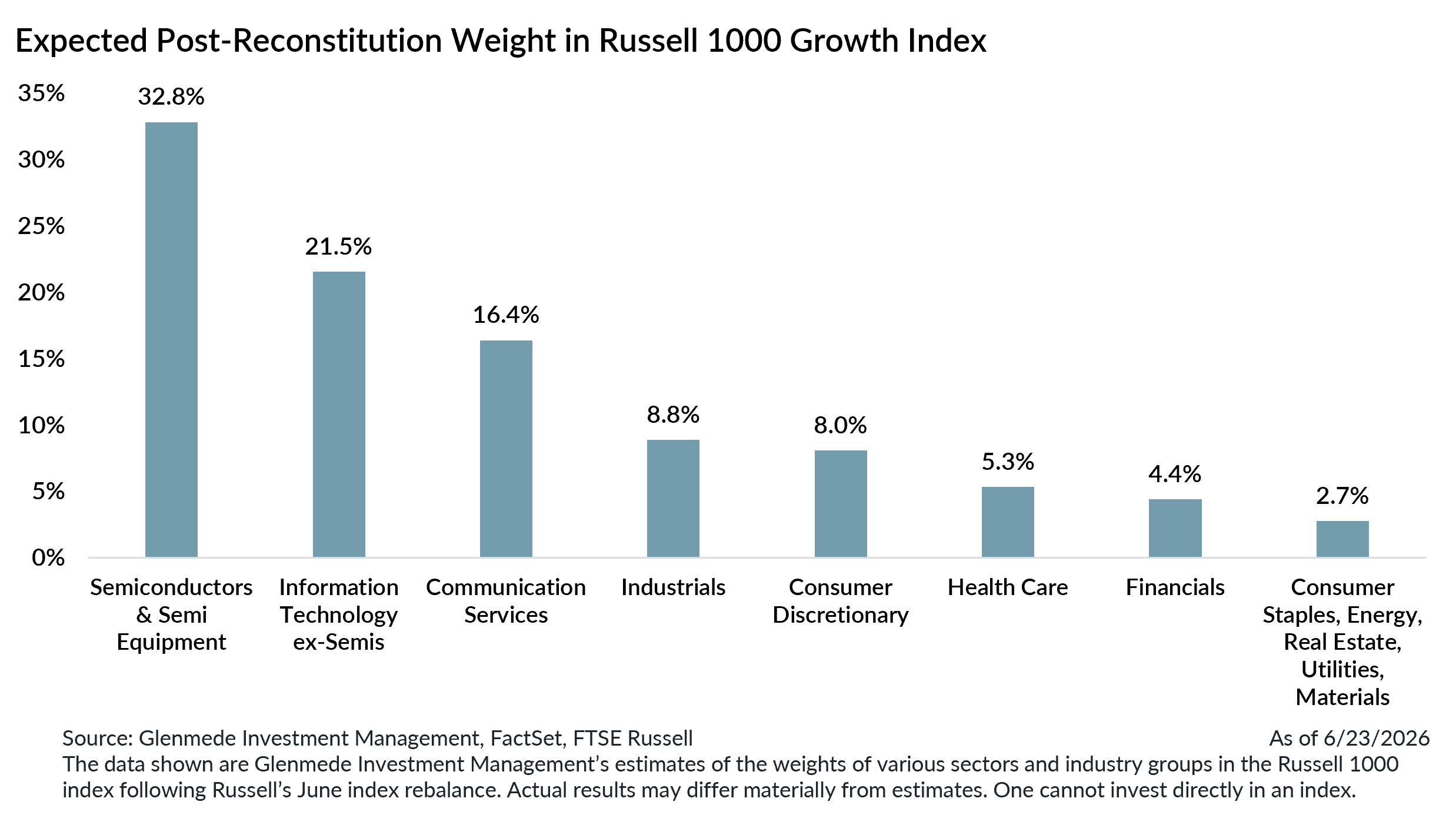

Growth-oriented benchmark indexes based on market capitalization are becoming more heavily exposed to this industry group. Semiconductors and semiconductor equipment are expected to represent almost a third of the Russell 1000 Growth Index after reconstitution. This would be about double the weight of communication services at 16.4% and meaningfully above the technology sector excluding semiconductors at 21.5%. Put another way, the semiconductor-related industry groups would carry a weighting more than 12 times greater than the consumer staples, energy, real estate, utilities, and materials sectors combined.

That composition has practical implications. Portfolios and benchmarks tied to Russell indexes may now carry greater sensitivity to semiconductor trends and all that comes with it, including capital expenditure cycles and technological advancements related to AI trends. At the same time, lower weights in software and hardware may reduce diversification benefits among technology stocks in the Russell 1000 Growth Index.

Index reconstitutions do not change underlying company fundamentals, but they can influence capital flows, portfolio construction, and risk concentrations. Passive strategies inherit these shifts by design. Active managers retain the flexibility to assess whether benchmark weight changes are supported by fundamentals, valuations, and risk exposures as market structure evolves.

Val deVassal, CFA

Portfolio Manager, Disciplined Equity,

Glenmede Investment Management

Alex Atanasiu, CFA

Portfolio Manager, Disciplined Equity

Glenmede Investment Management

David Marcucci, CFA

Client Portfolio Manager, Disciplined Equity

Glenmede Investment Management