Market Snapshot: Mega IPOs Meet Index Math

The U.S. IPO market appears to be gaining momentum, but not in the broad-based way that typically defines a classic issuance cycle. Rather than a surge in the number of companies coming public, this environment is being driven by a small group of exceptionally large deals. SpaceX, Anthropic, and OpenAI are expected to rank among the largest IPOs on record, with potential valuations and offering sizes that could push total capital raised to new highs despite a still-muted count of overall IPO activity.

Measured in dollars raised, this wave of issuance appears historically significant, but adjusting for the much larger size of today’s equity market, the impact appears less groundbreaking. IPO proceeds as a share of total U.S. equity market capitalization are expected to remain well below the extremes seen in prior cycles, suggesting that even a record-breaking year of capital raised may not represent the same degree of market-wide issuance pressure as earlier IPO booms, such as the late 1990s.

The index implications are more nuanced. Some index providers have shifted their rules to accommodate faster inclusion of large, high-profile IPOs. FTSE Russell, for example, has shortened the seasoning period for certain large new listings, while Nasdaq has also adjusted its process. S&P Dow Jones Indices, by contrast, has maintained its process, sticking with its profitability and seasoning requirements. As a result, these companies may enter some broad market benchmarks much sooner than others, creating a staggered path into passive portfolios.

Even where inclusion happens quickly, initial index weights should be limited by public float. These companies are expected to debut with relatively low levels of publicly available shares, as insiders, employees, and early investors remain subject to lockup restrictions. Because major equity indices generally weight companies based on float-adjusted market capitalization, the headline valuation of a mega IPO may not immediately translate into a full benchmark weight.

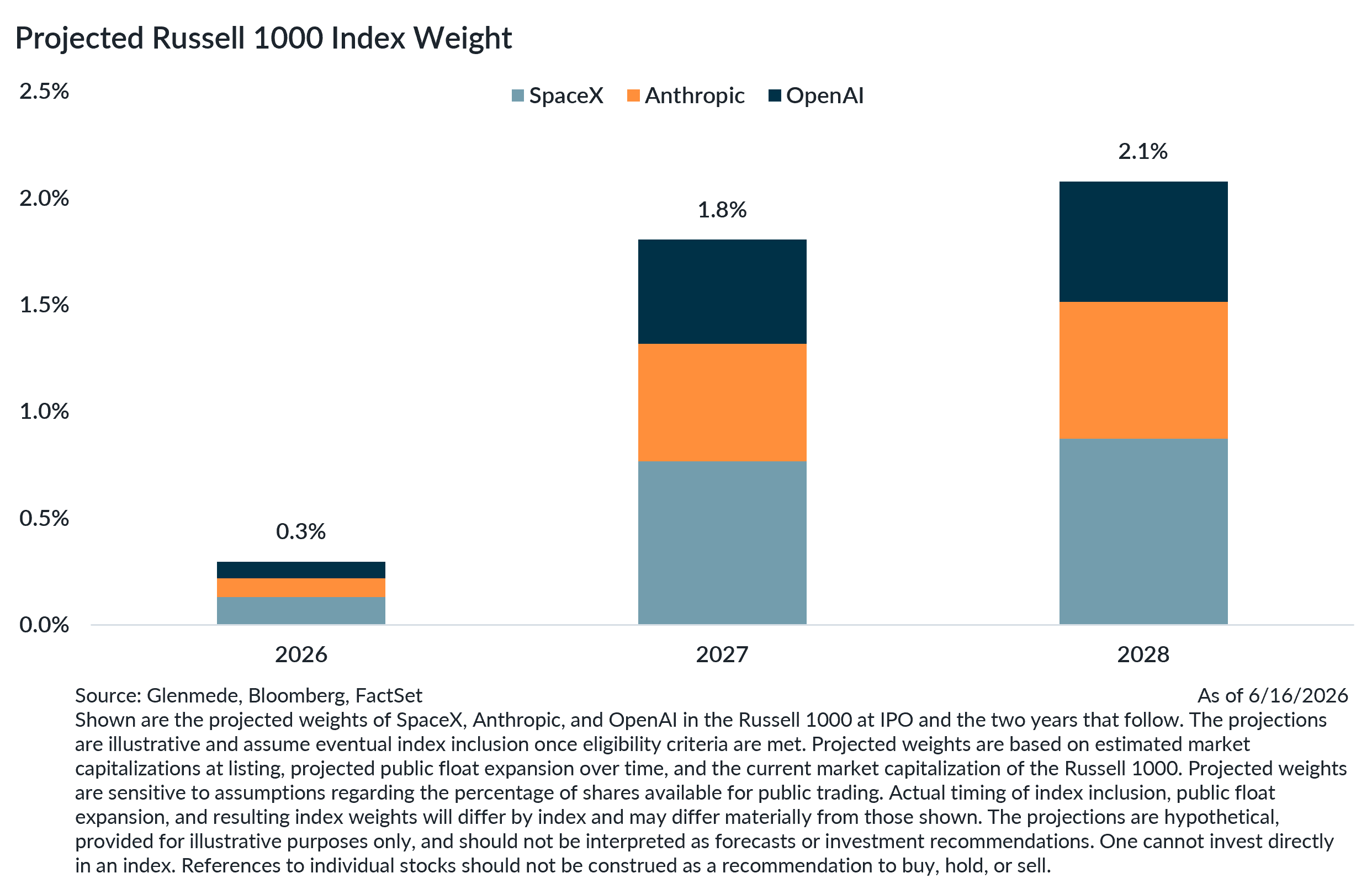

In practice, the combined weight of SpaceX, Anthropic, and OpenAI in the Russell 1000 index could be a mere 0.3% around initial inclusion, assuming the latter two follow through on plans to go public. This could rise to around 2% by the end of 2027 as lockups expire and public float expands. This projection relies on many assumptions around estimated market capitalizations at listing and the pace at which shares become publicly available, while also assuming the stocks perform in line with the rest of the index over that period. Actual weights could differ materially based on post-IPO stock performance, deal timing, final offering size, and the path of float expansion. Yet the observation remains that these massive companies may come to represent a smaller share of major indices in the short- to medium-term than many expect.

Despite record-setting headlines and media hype, this year’s mega cap IPOs are likely to affect broad equity indices only gradually over time. The market impact may be real, but it should build over the coming years through float expansion and index inclusion mechanics rather than arrive all at once.

Jason Pride, CFA

Chief of Investment Strategy and Research, Glenmede

Michael Reynolds, CFA

Vice President, Investment Strategy, Glenmede