The Quarterly Recap Q1 2026: Economic & Market Recap

Executive Summary:

- Geopolitical tensions, particularly the escalation in Iran, introduced a new source of uncertainty, though economic data remained broadly constructive with some modest signs of softening beneath the surface.

- A Supreme Court ruling reshaped the implementation of tariffs, while the Federal Reserve remained on hold as markets scaled back expectations for rate cuts.

- Equity markets lost momentum following a reversal in mega-cap leadership, though performance broadened beneath the surface with strength across smaller companies and international markets.

- Above-trend economic growth prospects remain intact, though risks from geopolitical developments, private credit, and elevated valuations warrant ongoing monitoring.

Geopolitics Take Center Stage

Geopolitical tensions moved to the forefront in Q1, introducing a new layer of uncertainty. Early-quarter developments in Venezuela and Greenland were ultimately overshadowed by an escalation in Iran, where risks to key energy transit routes raised concerns about potential disruptions to global oil and natural gas supply. While the full impact had yet to flow through to economic data, the conflict added a geopolitical risk premium into markets, with higher energy prices expected to place upward pressure on inflation and weigh on growth in the months ahead.

Against this backdrop, underlying economic data were generally constructive as distortions tied to the government shutdown in the prior quarter began to fade. Inflation remained relatively benign during the quarter, though higher energy prices had yet to fully work their way through to higher gasoline prices at the pump. The labor market continued to show signs of resilience, but with early indications of softening, including lighter payroll growth and a modest uptick in the unemployment rate. Taken together, conditions pointed to an economy that remained on stable footing, albeit with some modest but manageable cracks beneath the surface.

Advances in artificial intelligence continued to support optimism around accelerating productivity, even as concerns emerged around potential labor displacement for white collar workers and broader economic disruption. At the same time, scrutiny of private credit intensified, with loan markdowns, limited transparency, and the use of flexible financing structures raising questions about how risks may be building beneath the surface. While neither dynamic appeared likely to derail the expansion in the near term, both represented important areas to monitor as the cycle continued to evolve.

Policy in Transition

The Supreme Court ruled that tariffs implemented under the International Emergency Economic Powers Act were unlawful, though the practical impact was limited. A new set of tariffs were quickly announced via alternative authorities, and the administration initiated Section 301 investigations that could, over time, restore tariff policy to a similar pre-ruling shape and form. However, the status and timing of potential refunds tied to the original tariffs remained uncertain and subject to ongoing legal challenges. Meanwhile, a partial government shutdown persisted through much of the quarter.

The Federal Reserve remained on hold in Q1, making no changes to its policy rate as officials continued to balance risks to growth and inflation. Updated projections showed the median policymaker still expecting one rate cut this year, though market expectations shifted meaningfully over the quarter, with investors scaling back from anticipating two-to-three cuts to pricing in none. Leadership developments also drew attention, as the administration nominated Kevin Warsh to serve as the next Fed chair, with confirmation proceedings expected to begin in Q2. In parallel, a criminal investigation involving current Chair Jerome Powell added an additional layer of uncertainty around the Fed’s leadership outlook.

Rotations Within Equity Markets

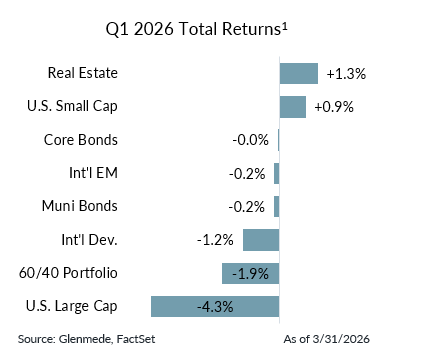

After several strong quarters in a row, equity markets lost some momentum in Q1. The S&P 500 declined 4.3%, driven in part by a reversal in leadership among mega cap stocks after years of outsized gains. Software stocks also faced pressure as investors reassessed how advances in artificial intelligence could disrupt existing business models. Beneath the surface, however, market leadership broadened meaningfully. The equal-weighted S&P 500 outperformed its market-cap-weighted counterpart by 5.0%, while small caps outpaced large caps by 5.2%. Within large caps, value stocks outperformed growth by 11.9% (based on Russell 1000 style indices), marking a notable shift after a prolonged period of growth dominance. International stocks outperformed, led by emerging markets. Japan stood out following renewed optimism around corporate governance reforms, while South Korea and Taiwan benefited from investor interest in AI-related opportunities outside the U.S. The price of gold increased 4.3% for the quarter but ended the quarter down 17% from its intra-quarter high. Bitcoin fell sharply, down 22%.

In fixed income markets, yields moved higher as inflation expectations picked up. The yield on 10-year U.S. Treasury bonds rose from 4.17% to 4.32%. Higher yields resulted in modestly negative total returns for both taxable and municipal investment-grade bonds. In lower-quality segments of the market, credit spreads widened modestly, reflecting a more cautious backdrop for risk assets.

Growth Accelerating, Risk Evolving

Looking ahead, the prospect for above-trend economic growth this year remains intact, though modest frictions have emerged from the conflict in Iran. Material net fiscal stimulus, waning tariff-related headwinds, and the potential for AI-driven productivity improvements appear likely to remain powerful forces supporting the ongoing economic expansion. While higher energy prices may weigh on growth, a recession appears unlikely at this stage, particularly given the U.S. economy’s increased energy independence relative to past crises. As a result, the economy should remain relatively resilient to an energy price shock, though the impact may be more pronounced in countries that are large net importers of energy. However, these developments will be important to monitor, particularly if further escalation leads to another jump higher in energy prices.

The conflict in Iran is not the only risk investors should be monitoring. Ongoing concerns in private credit, including signs of weakening discipline and limited transparency, bear watching for potential spillover into broader markets. On the other hand, given the underlying strength of the financial system and limited linkages through the banking channels, a systemic crisis appears unlikely. At the same time, elevated capital spending tied to artificial intelligence represents a significant bet on future demand, raising the risk that investment could outpace realized returns.

A constructive growth backdrop is tempered by still-elevated valuations in risk assets. While the recent pullback in growth stocks has narrowed valuation gaps, a meaningful disparity remains between mega cap stocks and the broader market. Small caps may continue to benefit from more reasonable relative valuations and greater sensitivity to an economy expected to grow above trend. Fixed income offers fairly priced yields and should continue to serve as a stabilizing force in portfolios.

1Asset classes are represented by the following: Large Cap (S&P 500), Small Cap (Russell 2000), Int’l Dev. (MSCI EAFE), Int’l EM (MSCI EM), Real Estate (FTSE EPRA/NAREIT Developed), Core Bonds (Bloomberg U.S. Aggregate), Muni Bonds (Bloomberg Municipal), 60/40 Portfolio (60% MSCI ACWI, 40% Bloomberg U.S. Aggregate). Past performance may not be indicative of future results. One cannot invest directly in an index.

This material was produced by Glenmede Investment Management, LP or its affiliate The Glenmede Trust Company, N.A. (collectively, “Glenmede”) for informational purposes and is not intended as personalized investment advice to purchase, sell or hold any investment or pursue any particular strategy. Opinions and analysis expressed in this material are those of the author or investment team as of the date of preparation and may change without this document being updated. Views expressed do not necessarily reflect the opinions of all investment personnel at Glenmede and may not be reflected in all the strategies and products offered. Forecasts or estimates provided herein, including those related to market outlook are based on research including publicly available information, internally developed data and third-party sources believed to be reliable, but accuracy cannot be guaranteed. Future results may differ significantly depending on market, security specific, economic or political conditions. Charts and graphs provided herein are for illustrative purposes only. Past performance is no guarantee of future results. Indexes mentioned are unmanaged and do not include any expenses, fees or sales charges. It is not possible to invest directly in an index. Any index referred to herein is the intellectual property (including registered trademarks) of the applicable licensor. Any product based on an index is in no way sponsored, endorsed, sold or promoted by the applicable licensor and it shall not have any liability with respect thereto. Financial intermediaries are only permitted to distribute this material in accordance with applicable law and regulation. Such financial intermediaries are required to satisfy themselves that the information in this material is appropriate for any person to whom they provide it. Glenmede shall not be liable for the use or misuse of this material by any such financial intermediary.