Thought Leadership

Insights

October 04, 2023

Insights

October 04, 2023

Market cap-weighted index funds reflect several risks to the investor. An experienced active manager can effectively reduce some of these risks with quantitative tools, a valuation discipline, fundamental research, and portfolio optimization techniques.

Insights

September 28, 2023

Insights

September 28, 2023

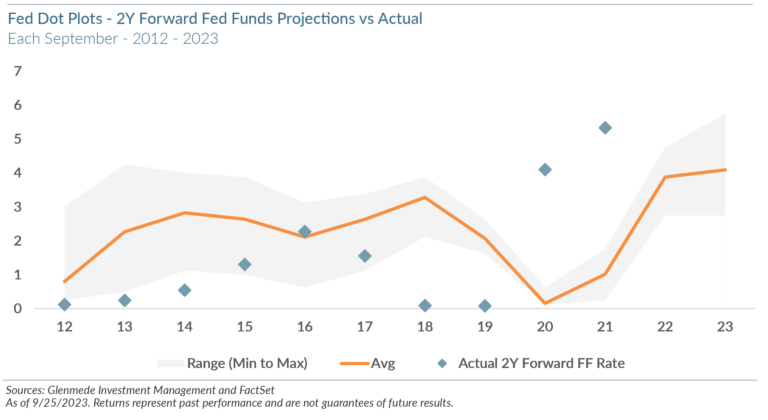

What’s Wrong With This Picture? The Fed’s dot plot is again causing a stir as investors try to glean wisdom about the long-term trajectory of interest rates. …

Insights

September 19, 2023

Insights

September 19, 2023

GIM Small Cap Portfolio Manager Jordan Irving reexamines the Russell 2000 Index concentration of negative earners and the outsized influence that the lower quality nature of recent Initial Public Offerings has exerted.

Insights

September 14, 2023

Insights

September 14, 2023

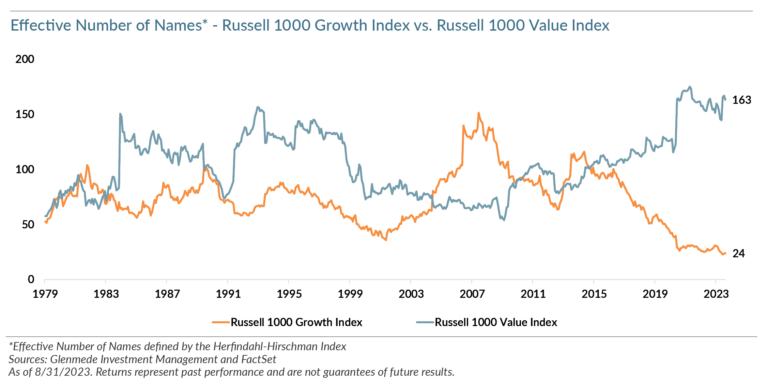

With the disparity of diversification between the Russell 1000 Growth and Value indices becoming more extreme, investors may want to seek active managers who can diversify away from these unprecedented levels of concentration. Learn more.

Insights

August 04, 2023

Historically, it was assumed that a higher cash reserve is a reflection of positive cash flows, indicates stability or at least a baseline level of liquidity, and that a higher proportion of CMV would indicate a discounted buying opportunity. However, research by the Quantitative Equity team at Glenmede Investment Management (GIM) has indicated that high proportions of cash or current assets to market value can actually be a proxy for higher volatility.

Insights

July 17, 2023

Insights

July 17, 2023

We are seeing unprecedented market concentration in broad-based indices.

Insights

May 03, 2023

Insights

May 03, 2023

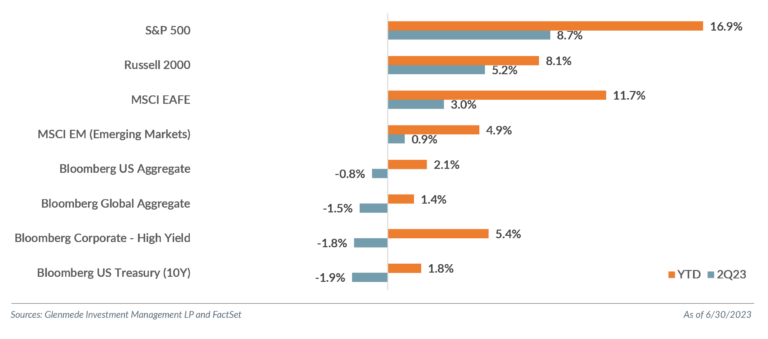

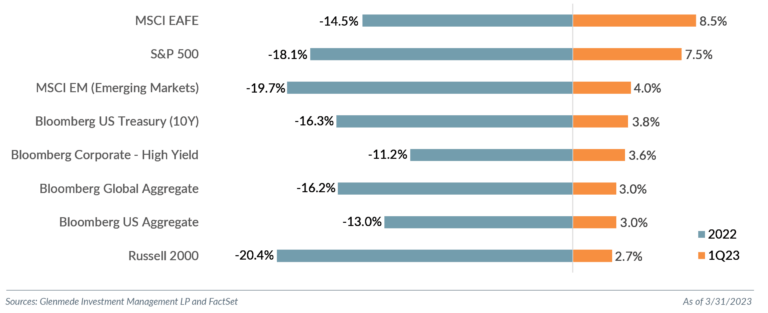

Equity markets rallied in Q1 2023, with much of what underperformed in 2022 reversing course to rebound sharply to start the year.

Our research suggests that it’s not just the presence of women in leadership positions, but broader gender equity characteristics that may contribute to stronger corporate performance.

Insights

February 28, 2022

Insights

February 28, 2022

We believe small cap stocks entered the correction phase of the negative earners’ outperformance in second-half 2021 and could continue to see relative weakness in these names throughout 2022.

Insights

February 23, 2022

Insights

February 23, 2022

We look at the current valuation of small caps and consider the potential behavioral implications that typically emerge during investment regime changes.