The Quarterly Statement Q4 2023: It’s A Small World After…2023

Market Review Fourth Quarter 2023

What We Know: Q4 2023 Recap

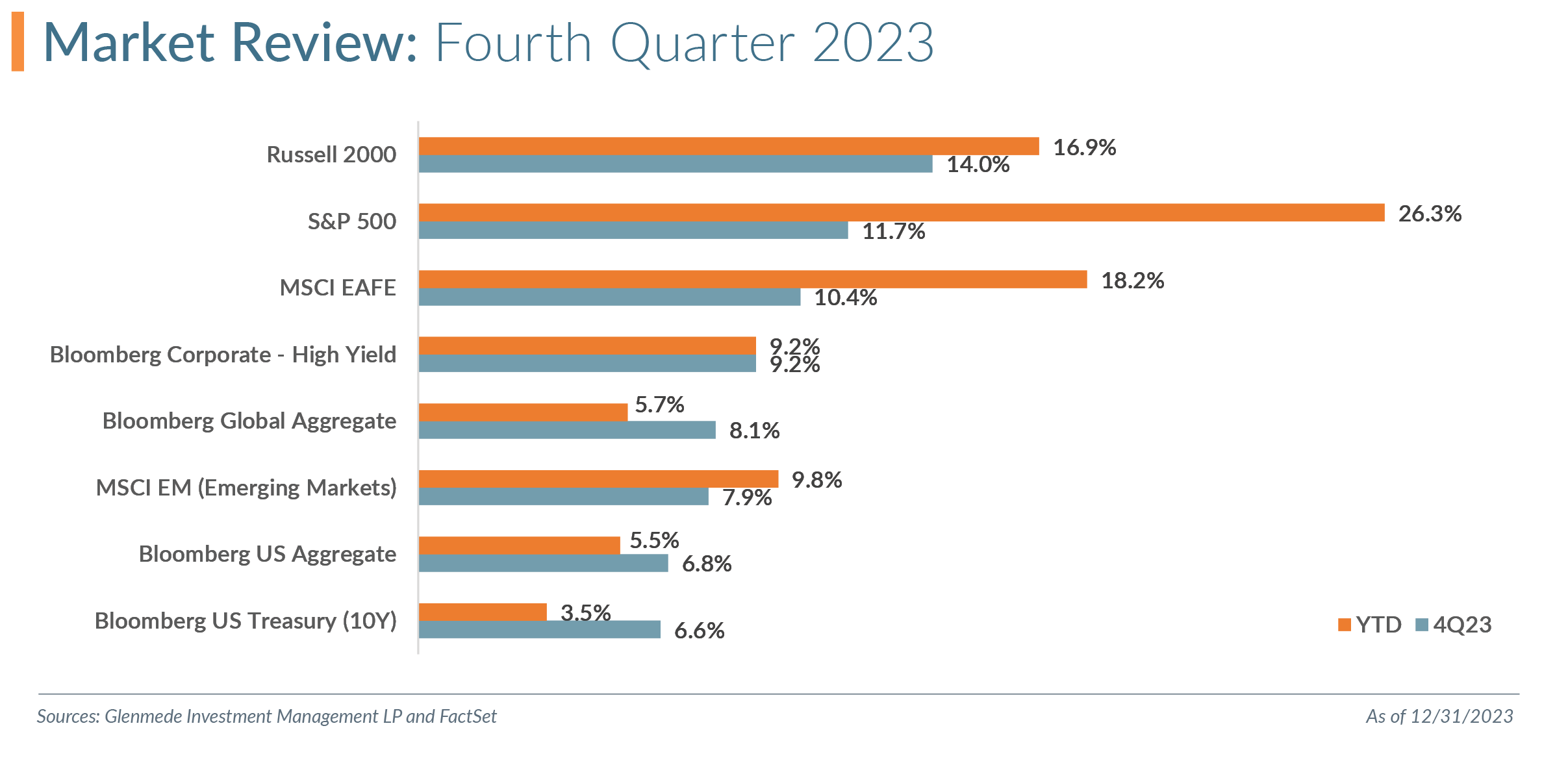

Markets saw a risk-on rally in both equities and fixed income in Q4 2023. Investor expectations of a soft landing rose under the assumption the Federal Open Market Committee (FOMC) would begin cutting rates, and potentially aggressively, in 2024. These views contrasted with investor concerns in the third quarter of an economic hard landing. This narrative shift led to broader equity participation in the November and December rally than experienced during most of the year. As of October 31, 2023, of the S&P 500’s 10.7% YTD total return, almost 100% was attributable to the “Magnificent Seven” (Apple Inc., Microsoft Corporation, Alphabet Inc., Amazon.com, Inc.,NVIDIA Corporation, Tesla, Inc. and Meta Platforms, Inc.). November and December saw the remainder of the S&P 500 provide more notable contributions, with 66% of the 11.7% total return for the quarter coming from stocks excluding the Magnificent Seven. While still an outlier year in terms of the concentration of performance, this late-year broader rally resulted in the Magnificent Seven at 62% of the S&P 500 total annual return of 26.3% versus the nearly 100% as of the end of October.

The FOMC met twice in Q4 2023 and kept the fed funds rate steady at 5.25%-5.50%. Investor expectations of potential Fed rate cuts were highly volatile in 2023, and almost always more dovish than Fed rhetoric. Before the December FOMC meeting, fed fund futures markets implied four to five 25 bps rate cuts in 2024, notably different from the Fed rhetoric of “higher for longer.” At the meeting, FOMC members updated projections for future rates, suggesting potentially three 25 bps cuts in 2024 instead of the previously implied two. This slightly more dovish shift drove the so-called “Great Monetary Pivot” of 2024 market sentiment, resulting in an equity and rate rally in Q4 2023.

The fixed income rally turned what was tracking to be an unprecedented three-year losing streak for fixed income to a small positive for 2023. The U.S. Treasury curve steepened in the quarter, with the 2Y rallying 79 bps to yield 4.25%, the 10Y rallying 69 bps to yield 3.88% and the 30Y rallying 67 bps to yield 4.03%. The U.S. Treasury 10Y-2Y yield spread, a much-watched recessionary indicator, steepened in the quarter to -37 bps after flattening to over -100 bps in the second quarter.

The Russell 1000 Value Index resumed its lag to the Russell 1000 Growth Index in the quarter with returns of 9.5% and 14.2%, respectively. Given mega caps’ contribution to growth’s performance YTD, value has experienced its second worst annual performance relative to growth since 1979. Value ended the year 31.2% behind growth (Russell 1000 Value YTD return of 11.5% versus Russell 1000 Growth of 42.7%), an all-time best performing year for Russell 1000 Growth.

The Real Estate sector was the top S&P 500 performer, returning 18.8% for the quarter, its third best performance behind Q2 and Q3 2009, and bringing the YTD total return to 12.6%. Information Technology, 17.2%, and Financials, 14.0%, were the next two best performing sectors. Information Technology was the top-performing sector for the year with a total return of 57.8%, followed by Communication Services, 55.8% (both sectors have Magnificent Seven contributors). Energy was the only negative performing sector in the quarter with a -6.9% decline, ending the year with a -1.3% return. As part of the broader participation rally, small caps’ (Russell 2000 Index) total return of 14.0% outperformed large cap (S&P 500) in the quarter for the first time since Q3 2022. Small cap underperformed large cap for the third consecutive year and for six out of the past seven years (Russell 2000 total return of 16.9% versus S&P 500 of 26.3%). Small cap value (Russell 2000 Value Index) outperformed growth (Russell 2000 Growth Index) for the second quarter in a row, 15.3% versus 12.7%, but still finished the year lagging growth by 4.0% (Russell 2000 Value Index, 14.6%, versus Russell 2000 Growth Index, 18.6%).

International markets were positive in the quarter but still lagged their domestic counterparts. Developed international (MSCI EAFE Index) returned 10.4%, and international emerging markets (MSCI Emerging Markets Index) returned 7.9%. Both finished the year in positive territory, with the MSCI EAFE Index returning 18.2% and MSCI Emerging Markets Index, 9.8%.

What We Debate: A Practitioner’s Perspective – All Small

“When most people think about the future, they ignore that the future is a distribution of possibilities.” – Howard Marks

In a year dominated by inflation concerns, Fed rate debates, a banking crisis and an artificial intelligence frenzy, we highlight several charts that we believe reflect some of the more unusual market observations from 2023 and some thoughts for 2024 and beyond. Spoiler alert: We believe small will matter in both large cap and small cap.

U.S. Large Cap: 2023 Concentration

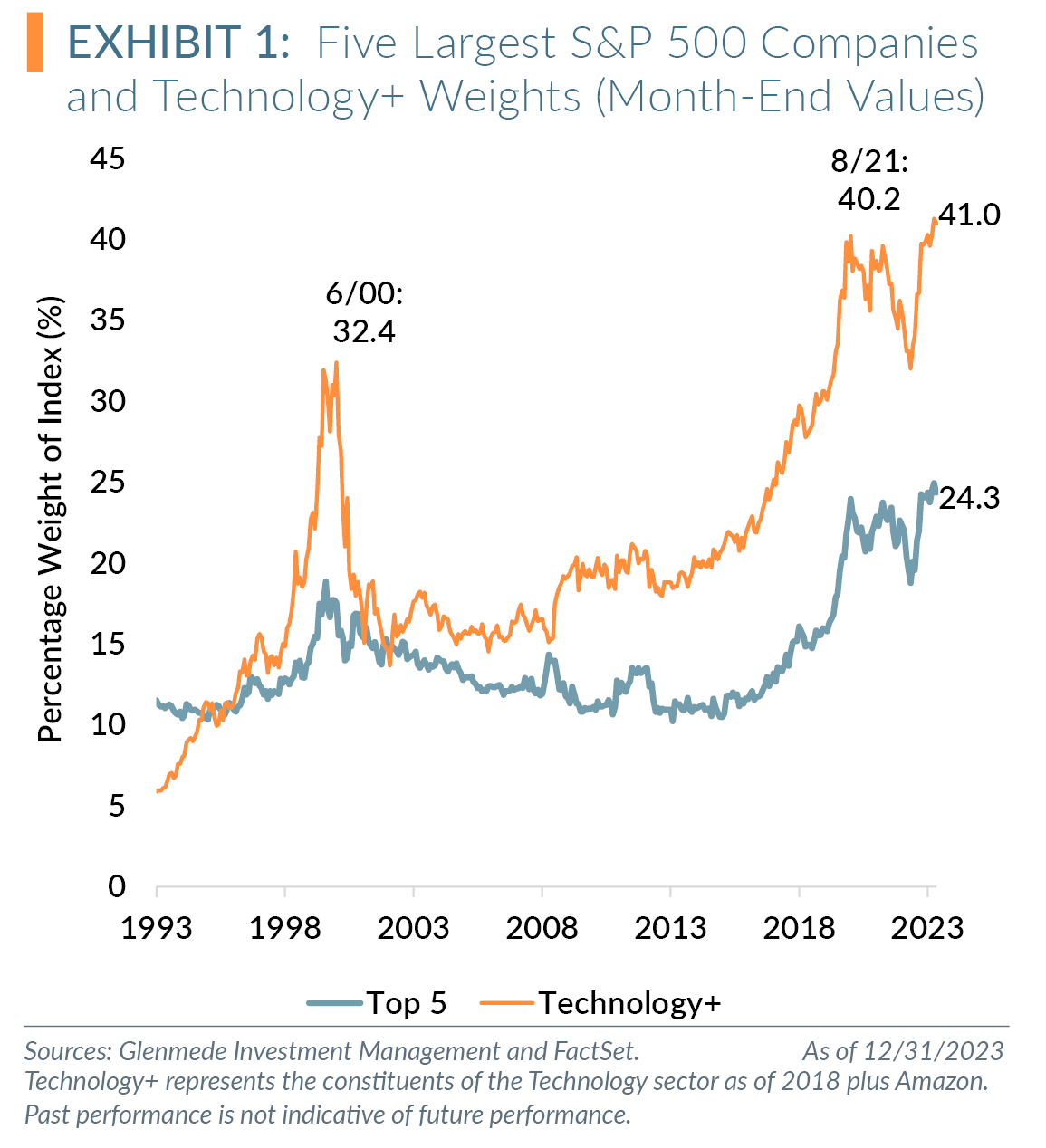

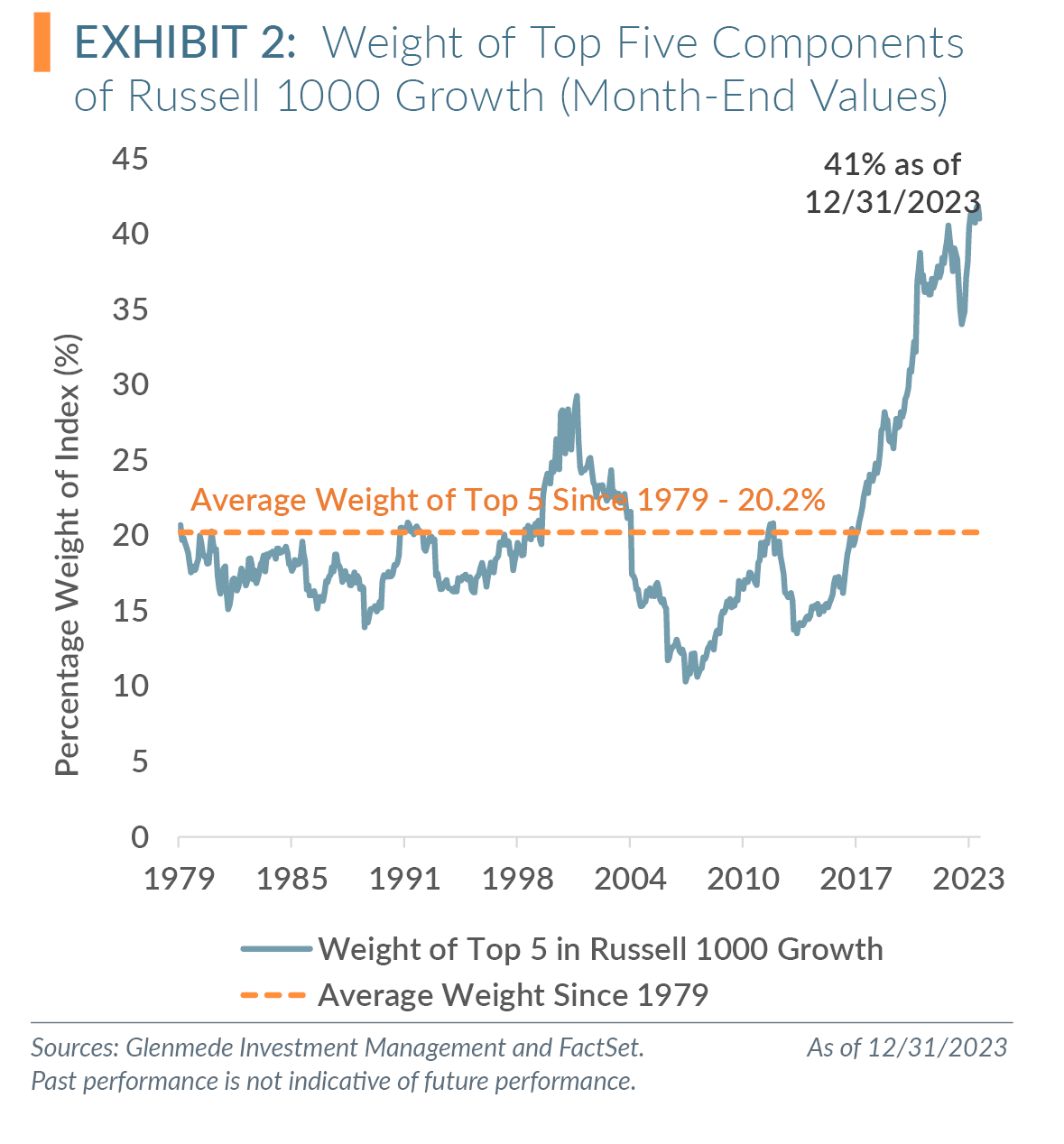

We have repeatedly discussed the increase in market concentration¹ for U.S. large cap stocks and the potential concentration risk for investors in large cap passive strategies. As shown in Exhibit 1, the top five weights of the S&P 500 accounted for 24.3% of the index, marking some of the greatest concentration for the S&P 500 in the past 60 years. Technology+ (Technology sector as of 2018 plus Amazon) finished the year at 41.0% of the index, the second highest monthly recording since 1993. As shown in Exhibit 2, the Russell 1000 Growth Index saw the highest concentration on record, with the top five component weights accounting for more than 41% of the index. The seven most concentrated readings for the Russell 1000 Growth all occurred in the last seven months of 2023, with the peak concentration in November 2023 at 41.9%.

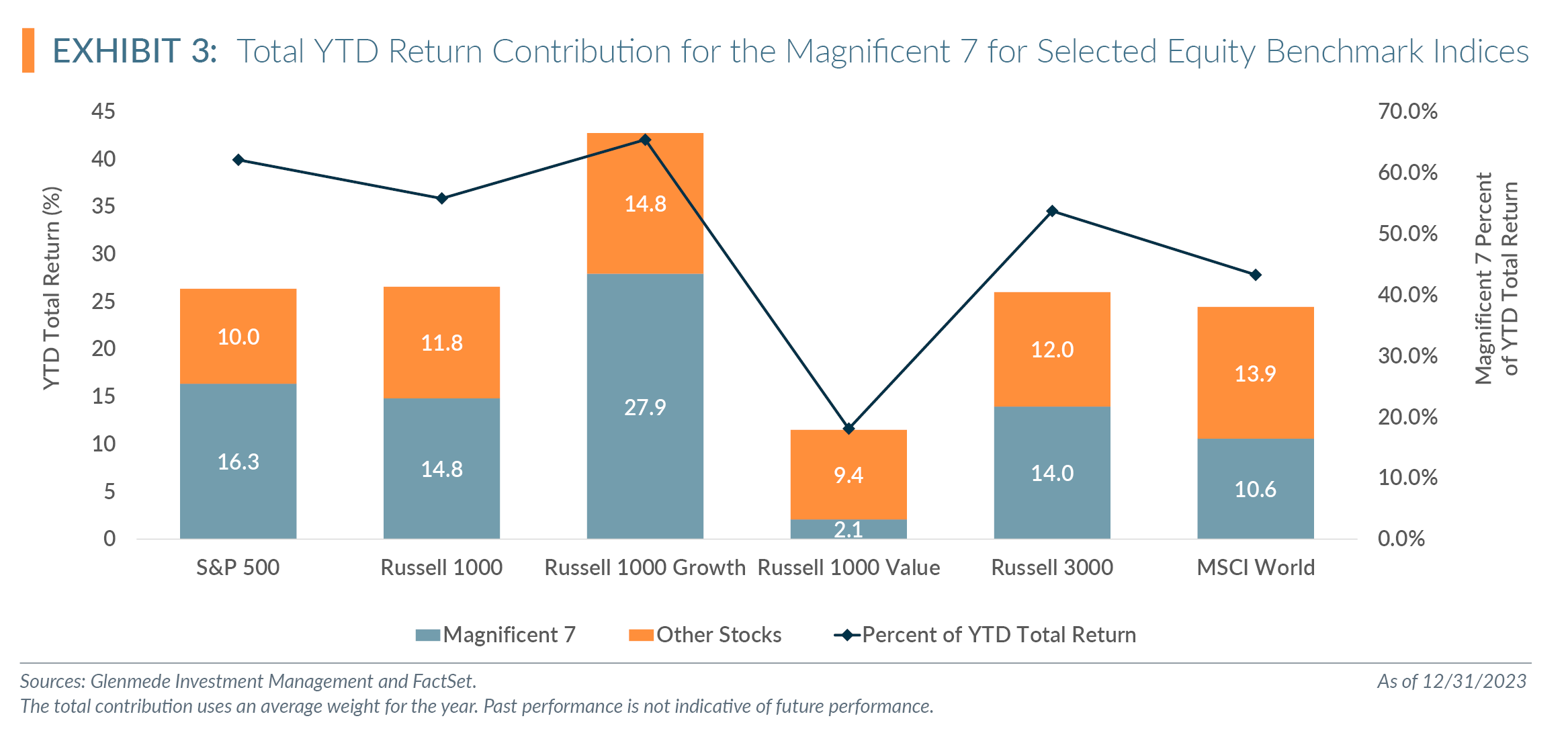

However, investor focus moved past just the top five weights, and the introduction of the Magnificent Seven was the story, accounting for a weighting of 28.2% of the S&P 500 and 47.2% of the Russell 1000 Growth Index. On the surface, the S&P 500 total return of 26.3% suggested a strong year (6th best performance over the past 25 years and 13th best over the past 50 years). However, like the index, the performance was concentrated. As shown in Exhibit 3, the Magnificent Seven performance accounted for a notable portion of several major indices’ total returns (S&P 500, Russell 1000, Russell 1000 Growth, Russell 1000 Value, Russell 3000 and MSCI World), ranging from 18.1% for the Russell 1000 Value to 65.8% for the Russell 1000 Growth, with the average contribution of 49.7% for the six indices.

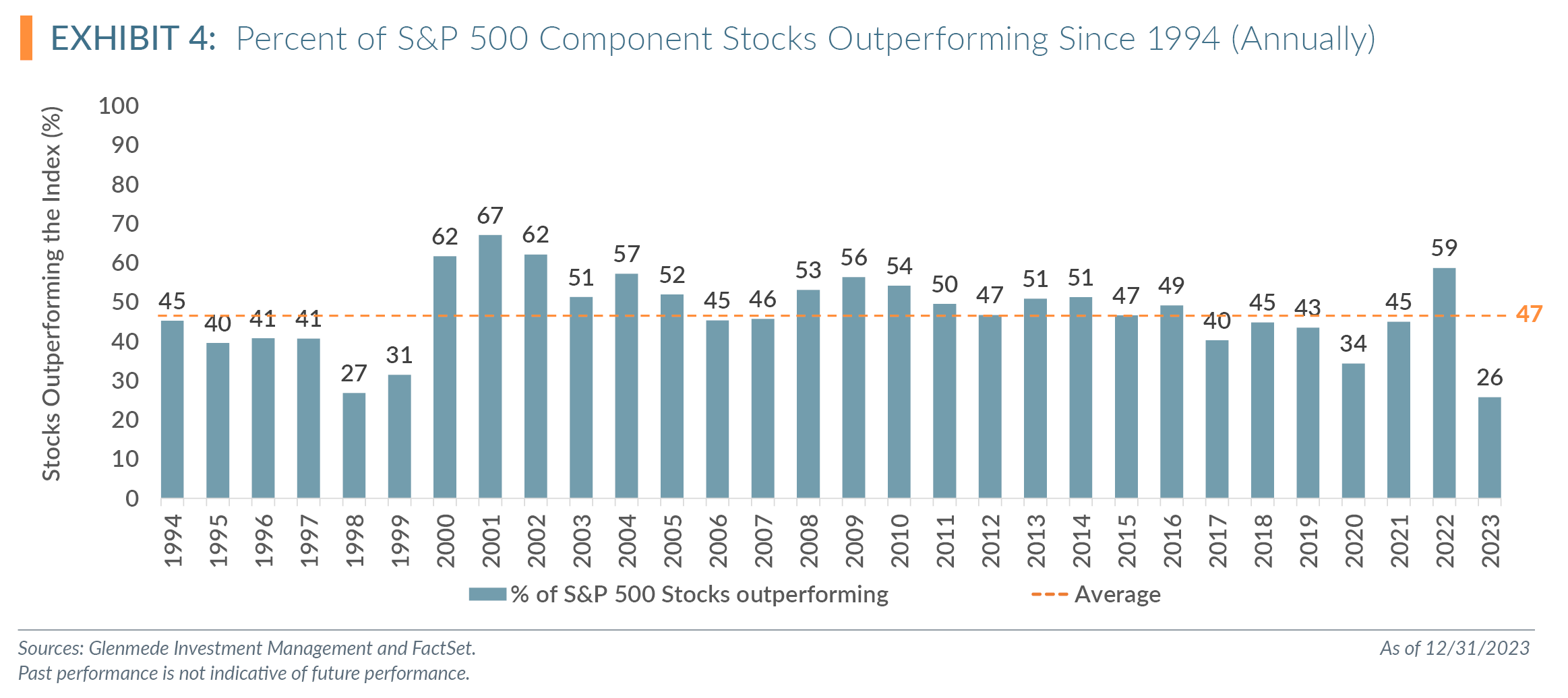

This concentration led to the lowest percentage of S&P 500 component stocks in the past 30 years beating the index for the year, as shown in Exhibit 4. This year had even less breadth than the peak of the dot-com years in 1998 and 1999.

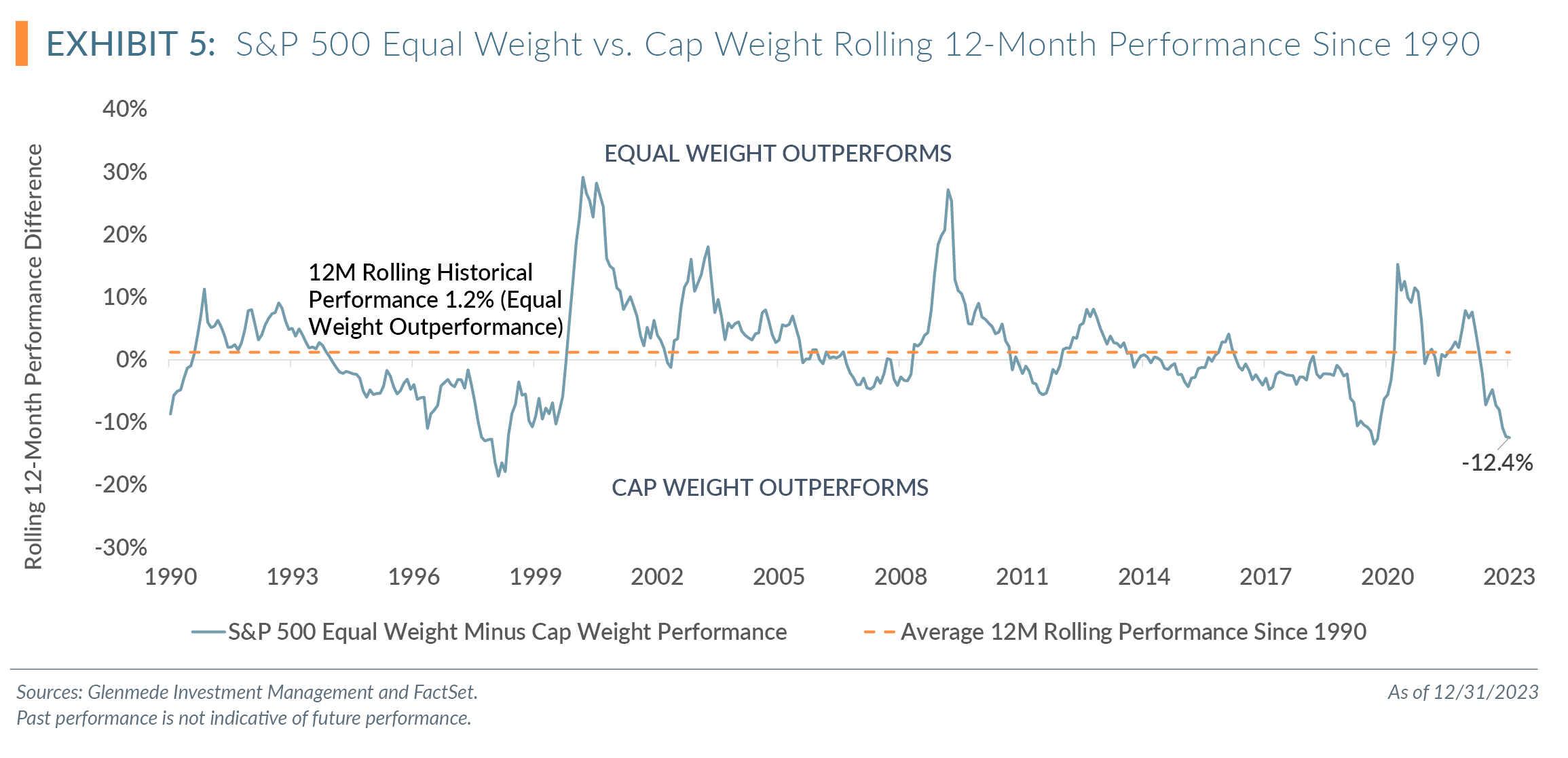

The concentration of the Magnificent 7 led to the 10th worst 12-month rolling performance of the S&P 500 Equal Weight versus Cap Weighted since 1990 and the second worst calendar year performance since 1990, as shown in Exhibit 5.

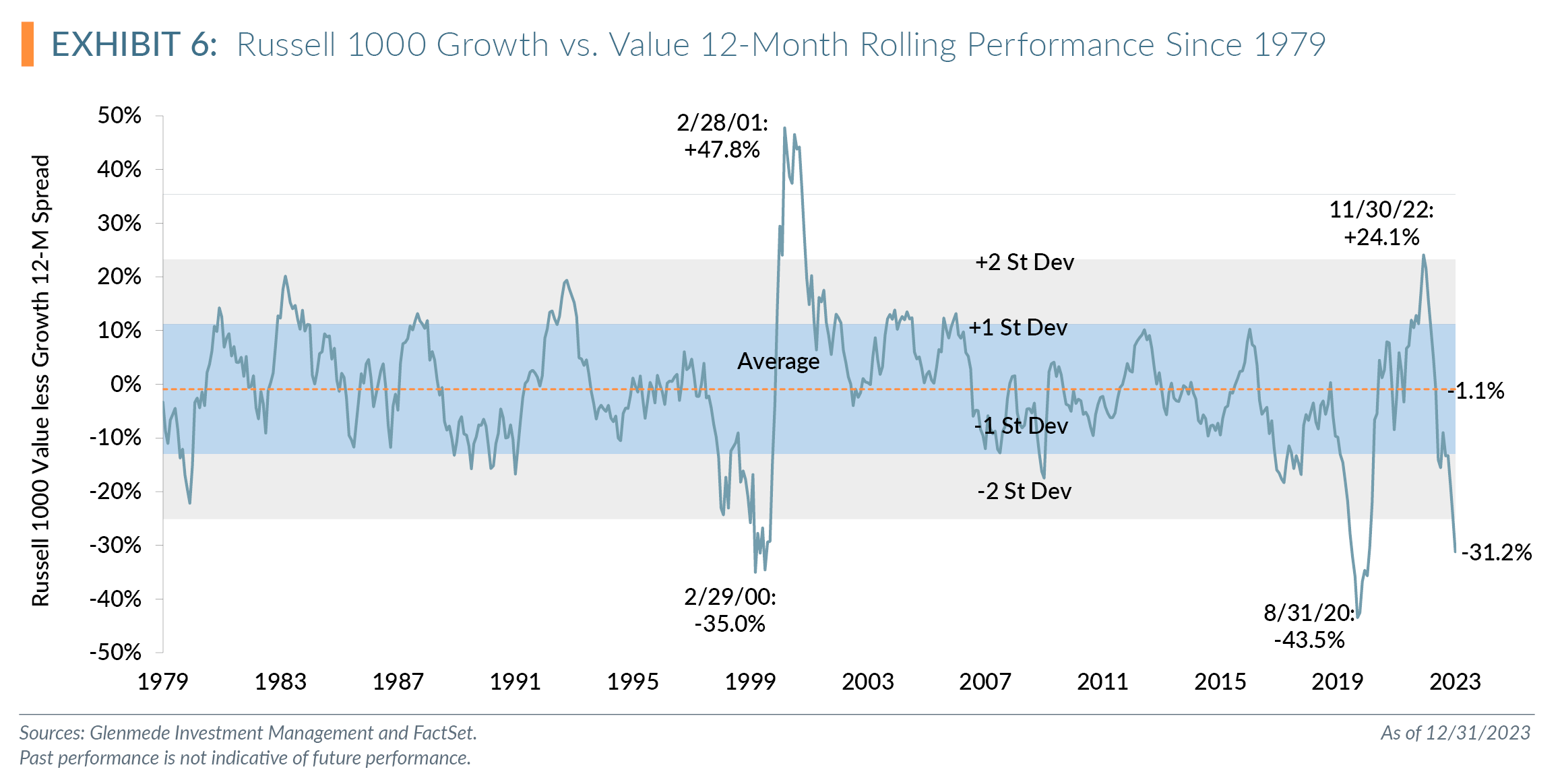

With the Magnificent 7 containing growth-focused companies, the Russell 1000 Value versus Russell 1000 Growth saw its 11th worst 12-month rolling performance dispersion since 1979 and its second worst calendar year performance in 45 years, as shown in Exhibit 6.

U.S. Large Cap: 2024 & Beyond

Given the cyclicality of value and growth (Exhibit 6), a mean reversion seems a logical prediction. A notable observation from this cycle is that the more extreme the dislocation, the more extreme the normalization, or snapback of performance of value relative to growth.

In the early 2000s during the dot-com exuberance, growth outperformed value within a 12-month rolling cycle by 35% ending February 2000. Value outperformed growth by 47.8% over the next 12-month rolling period. Following the unprecedented monetary and fiscal support during the COVID lockdowns in 2020, growth outperformed value by 43.8% on a rolling 12-month basis ending August 2020. Value outperformed growth by 7.9% over the next 12 months, and outperformed by over 13.5% on an average annualized basis over the next 28 months ending December 2022.

Our concern is that the significant shift to passive investing in large cap over the past decade may leave many investors wrong-sided for the snapback given the growth tilt of large cap passive indices. While the growth outperformance cycle could continue to stretch for a bit longer, we believe the current risk/reward is similar to a rubber band; that is, the growth cycle could continue to stretch, but the snapback of value will likely be quick and difficult to time. We believe investors can diversify the concentration risk and potentially participate in the value snapback by beginning to reallocate some passive large cap allocations to more actively managed strategies with relative underweightings to the concentrated stocks and a valuation disciplined approach.

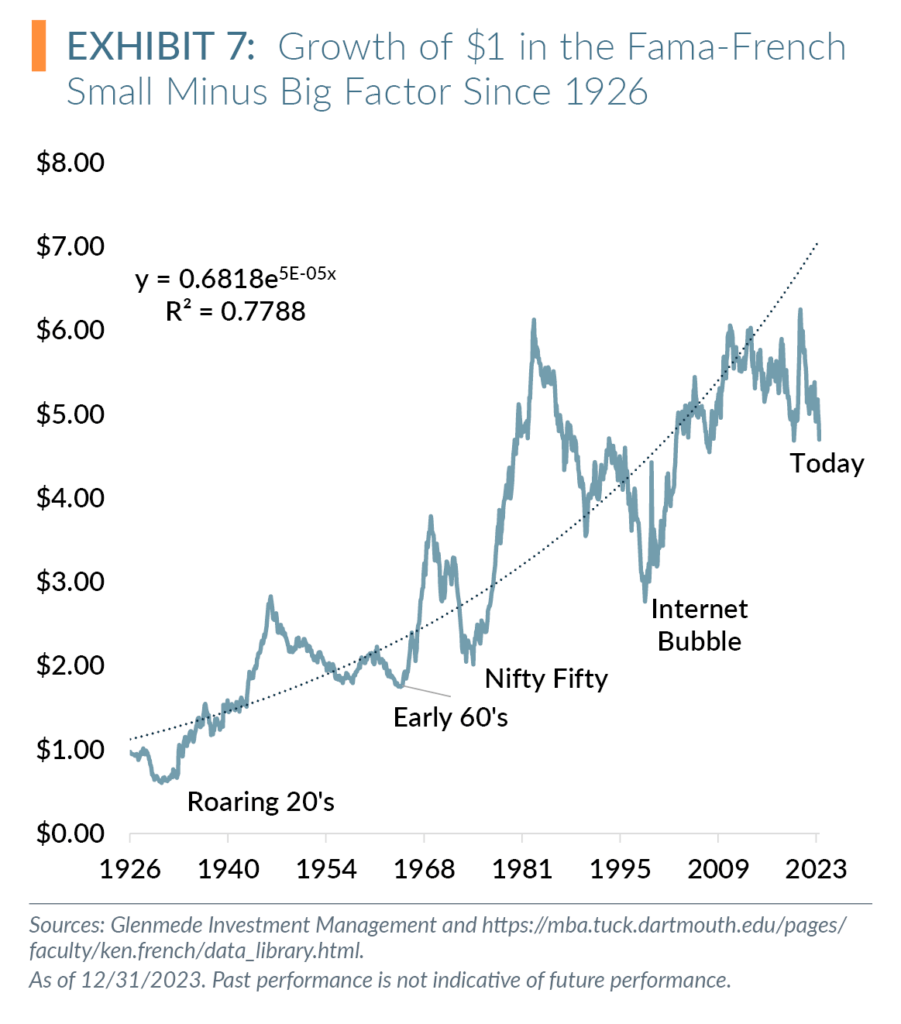

We also expect to see the resurgence of the size factor in 2024 and beyond. The size factor refers to the small minus big (SMB) factor in the Fama-French² Three-Factor Model showing that small companies outperform large companies over the longer term. Interestingly, like most things in the market, this factor is cyclical. In Exhibit 7, we show the growth of a $1 in the Fama-French SMB factor since 1926 with an exponential trend line. Over the past 97 years, there were five distinct periods where the factor underperformed by more than 20% from the trend line, as labeled on the chart: the Roaring 20s, Early 60s, Nifty Fifty, Internet Bubble and the current cycle.

In the previous four periods with dislocations of more than 20% below the trend line, over the next five years the factor showed an average 98.8% outperformance, or approximately 20% annualized outperformance.

Like all cycles, we cannot say with certainty that we are at the peak of the SMB factor deviation or that a reversion will occur. However, in the investment world of probabilistic outcomes, we believe having exposure to strategies that incorporate the size factor offers an attractive risk/reward for 2024 and beyond.

2024 and More Thoughts

We believe the Fama-French size factor begins to normalize and strategies that overweight exposure to smaller, attractively valued companies will outperform strategies with concentration to the largest, more expensive companies.

U.S. Small Cap: 2023 & Before Underperformance

In our Q3 2023 Quarterly Statement, we discussed why we believed an allocation to small cap was attractive, even with some economists still stoking recession fears. While Q4 2023 saw a rebound of small cap, with the Russell 2000 outperforming the S&P 500 for the first time in five quarters, we continue to believe small cap has room to run.

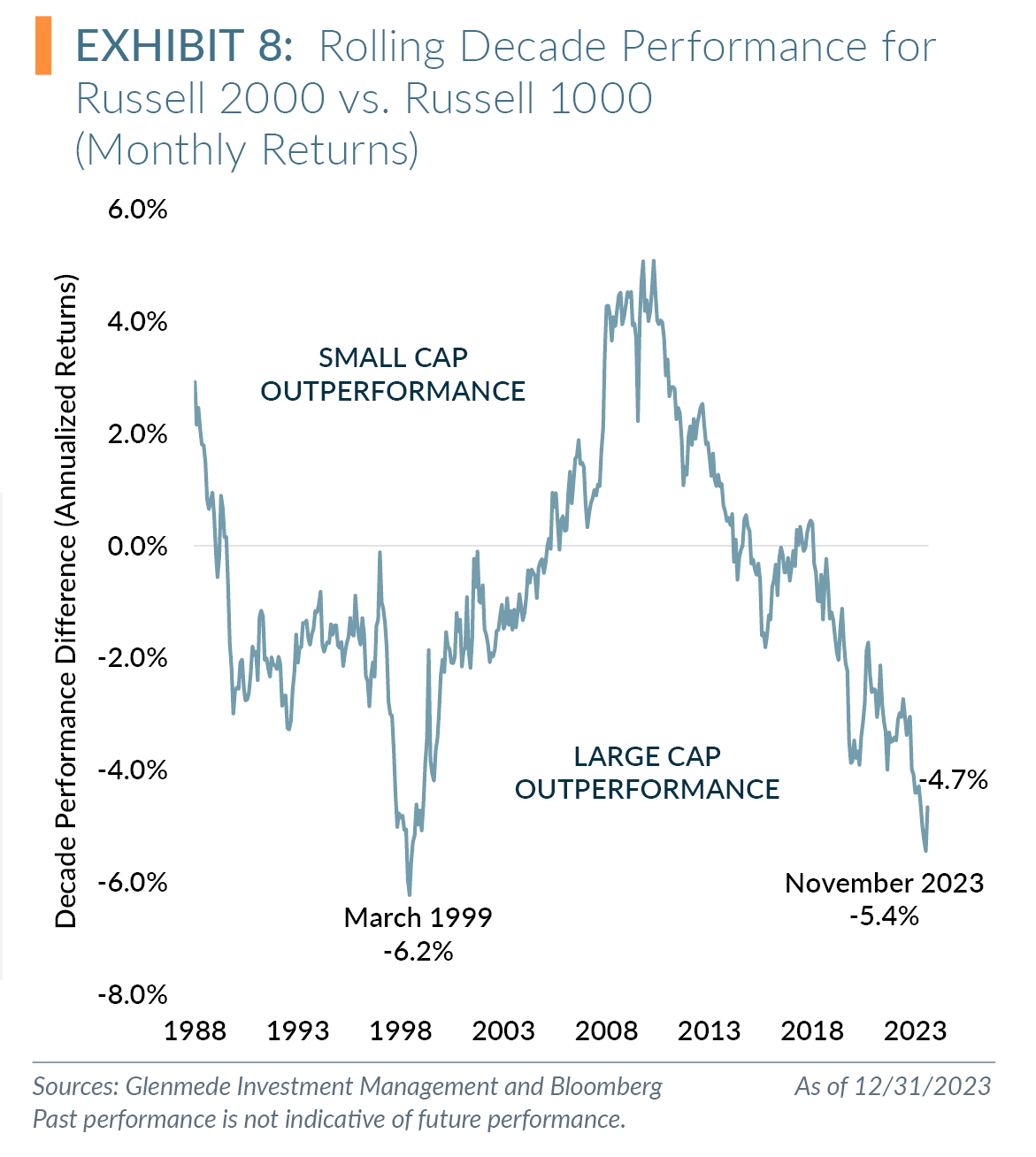

November 2023 hit an underperformance level of small cap (Russell 2000) relative to large cap (Russell 1000) that markets have not experienced since the dot-com era. Small cap performance has lagged large cap for years. For the decade ending November 2023, small cap underperformed large cap by 5.4% (annualized returns for the previous decade). Even with the Q4 2023 rally, small cap finished the year with an underperformance of 4.7% average annualized return over the past decade, as shown in Exhibit 8.

This long period of small cap underperformance rivals the underperformance of small cap during the dot-com boom, which saw a peak 6.2% average annualized return underperformance for the decade ending March 1999. For the next decade, small cap outperformed large cap by 4.5% annualized return. This next decade included the financial crisis in 2008 and 2009. From March 1999 through March 2007, small cap’s annualized outperformance of large cap was almost 7%.

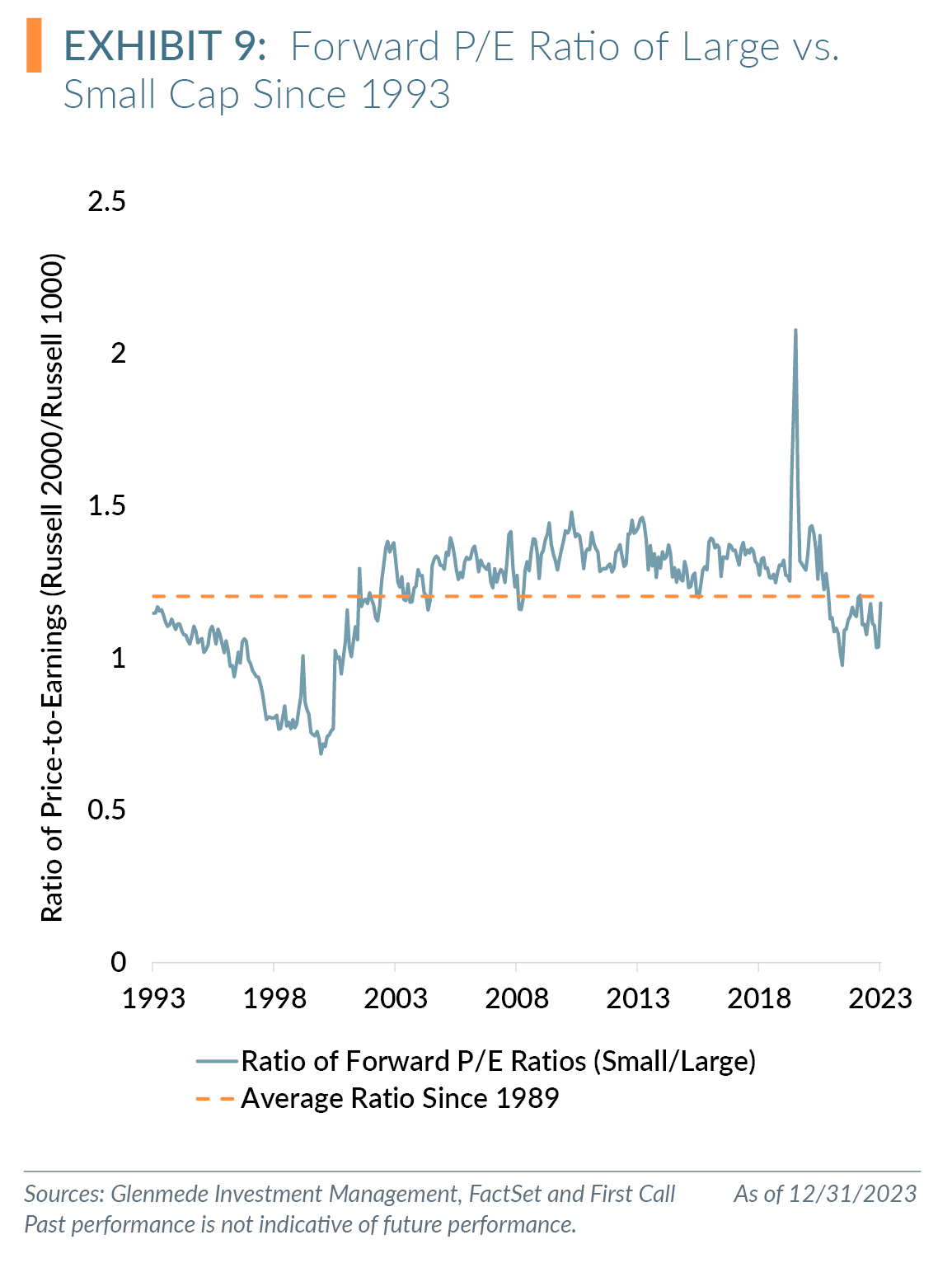

Valuations are signaling small cap attractiveness relative to large cap. Exhibit 9 shows the ratio of small cap (Russell 2000) to large cap (Russell 1000) forward price-to-earnings (P/E) ratios. The current ratio of P/E values of small-to-large of 1.18 is in the 37th percentile of observations over the past 30 years. The Russell 1000 forward P/E ratio is at 20.4x compared to the Russell 2000 forward P/E ratio at 24.0x, in the 81st and 89th percentiles, respectively, over the past 30 years. While this ratio is arguably a more attractive starting point than average, the ratio certainly is not near historical lows, which may beg the question as to why we continue to argue that small cap offers a relative attractive risk/reward.

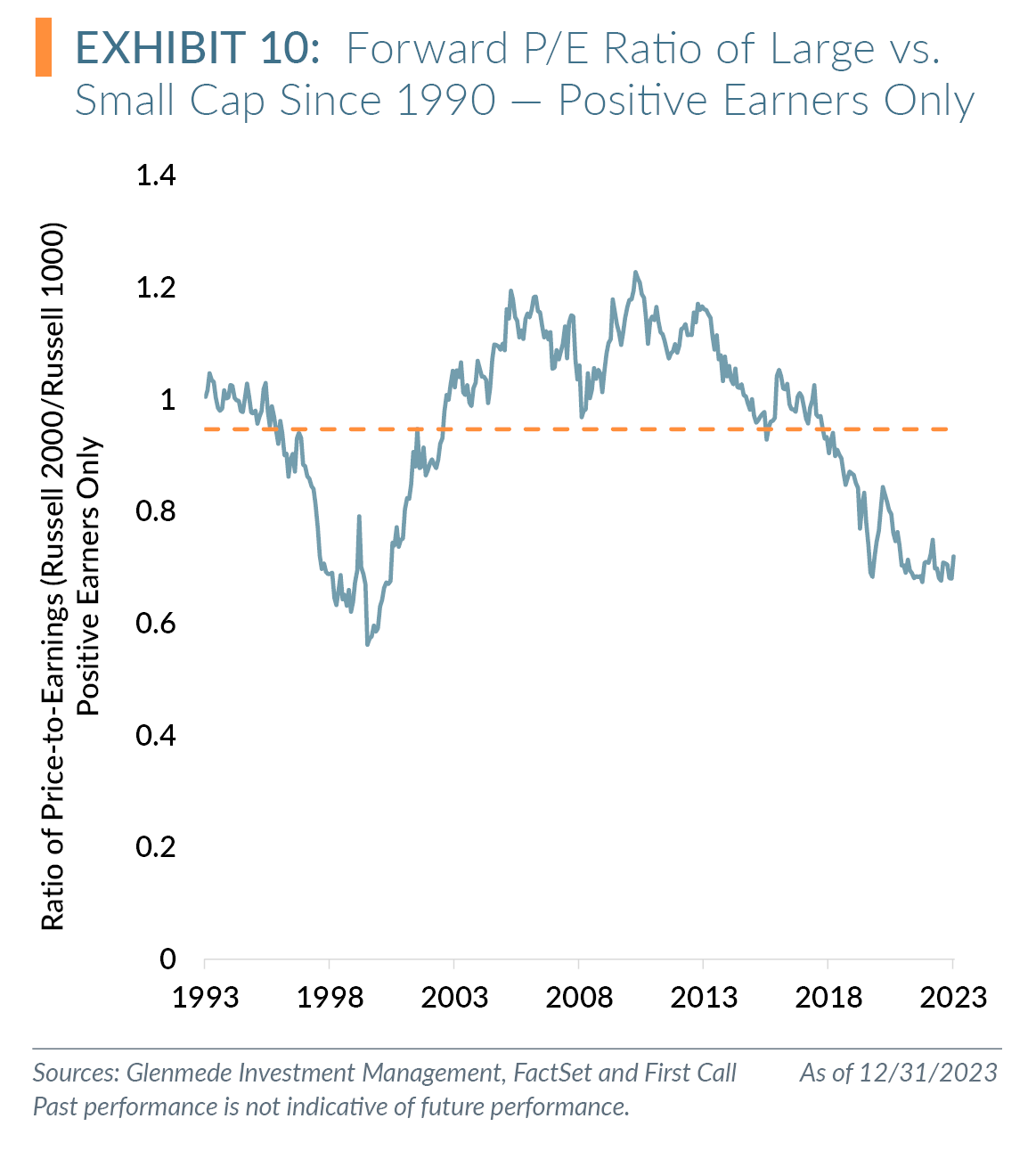

We believe there are areas of small cap that are more attractive than allocating to a passive index. Approximately 26% of Russell 2000 constituents ended the year as negative earners,³ which we believe offers a less attractive risk/reward for long-term growth. We continue to believe the best opportunity in small caps is a portfolio of positive earning, attractively valued companies. Exhibit 10 compares the ratio of the forward P/E of small cap (Russell 2000) to large cap (Russell 1000), filtering out negative earners. At 0.72, this ratio is near its dot-com euphoria level and in the 17th percentile over the past 30 years. When filtering out negative earners, the Russell 1000, with 20.0x forward P/E, is in the 83rd percentile of observations since 1993, while the Russell 2000 at 14.4x is in the 32nd percentile. Given our belief that starting points matter for future returns, the current relative value of this ratio suggests that the risk/reward for exposure to positive-earning small cap companies versus large cap is at one of the more attractive levels of the past 30 years.

An astute reader may wonder why we discuss growth versus value in large cap but focus more on core/blend strategies in small cap. Small cap is typically a smaller portion of an asset allocation model, with many investors using a single manager to gain exposure to the space. Of the Russell 3000 Index, which accounts for 96% of the investable U.S. stock market, the Russell 2000 accounts for 7% of the universe, according to the respective FTSE Russell factsheets. For a traditional 60% stock/40% bond portfolio that has no size tilts and only U.S. exposure, the allocation to small cap would be less than 5%. We believe an active core manager that allows the flexibility to tilt exposure to either style class versus trying to tactically market time the cycle or doing a 50/50 blend is a more attractive solution.

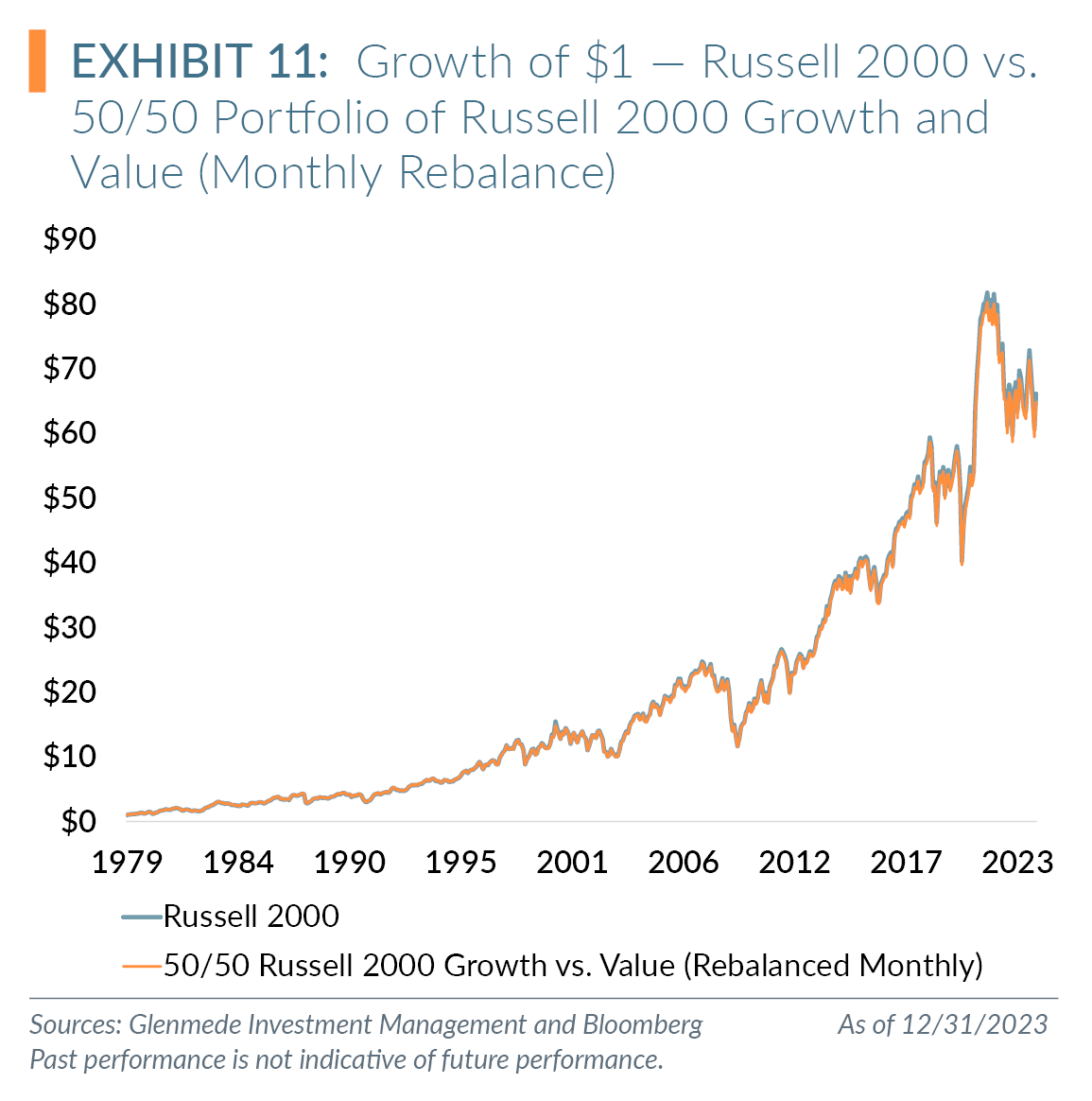

In Exhibit 11, we compare the growth of $1 of the Russell 2000 versus a 50/50 blend of Russell 2000 Growth and Value rebalanced monthly since 1979. The performance looks almost identical, with the blend returning an average annualized return of 10.0% compared to the monthly rebalanced portfolio’s average annualized return of 10.0%. This is obviously exclusive of transaction costs, which would of course be higher for the monthly rebalanced portfolio with a similar return.

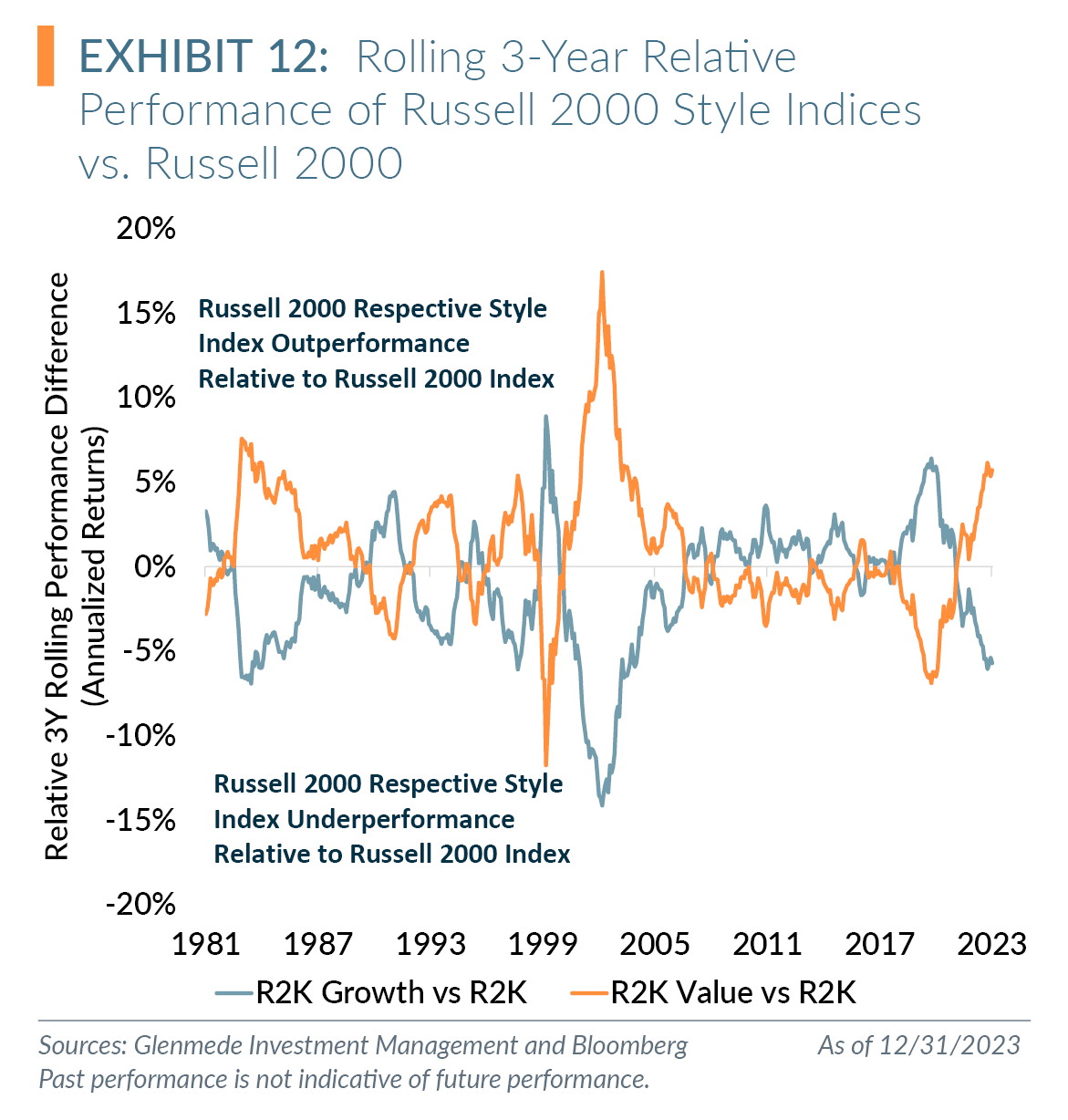

In Exhibit 12, we compare the three-year rolling annualized return of the Russell 2000 Growth and Value indices versus the Russell 2000 Index, creating a visual of the periods of style outperformance versus a core portfolio. While each style has various periods when it outperforms core, perfectly timing these periods is difficult. Following a single style-based approach may prevent exposure to or force a reallocation of capital from a more attractive opportunity if it does not fall within the specific style bucket. Allocating to an active core manager who can tilt more growth or value based on attractive risk/reward profiles rather than style boxes can reduce the risk of style commitment while maintaining the appropriate risk-adjusted exposures over a full market cycle.

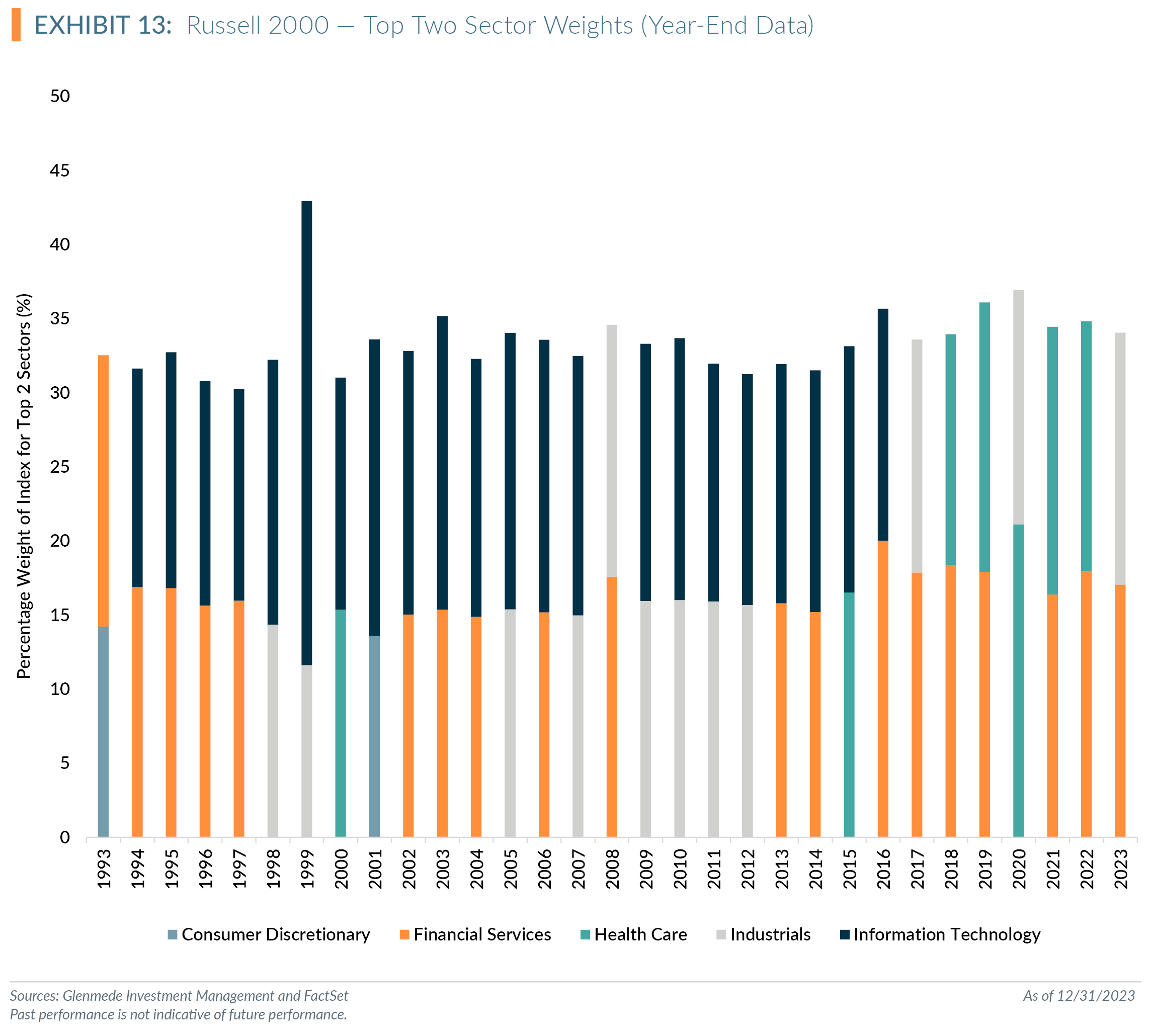

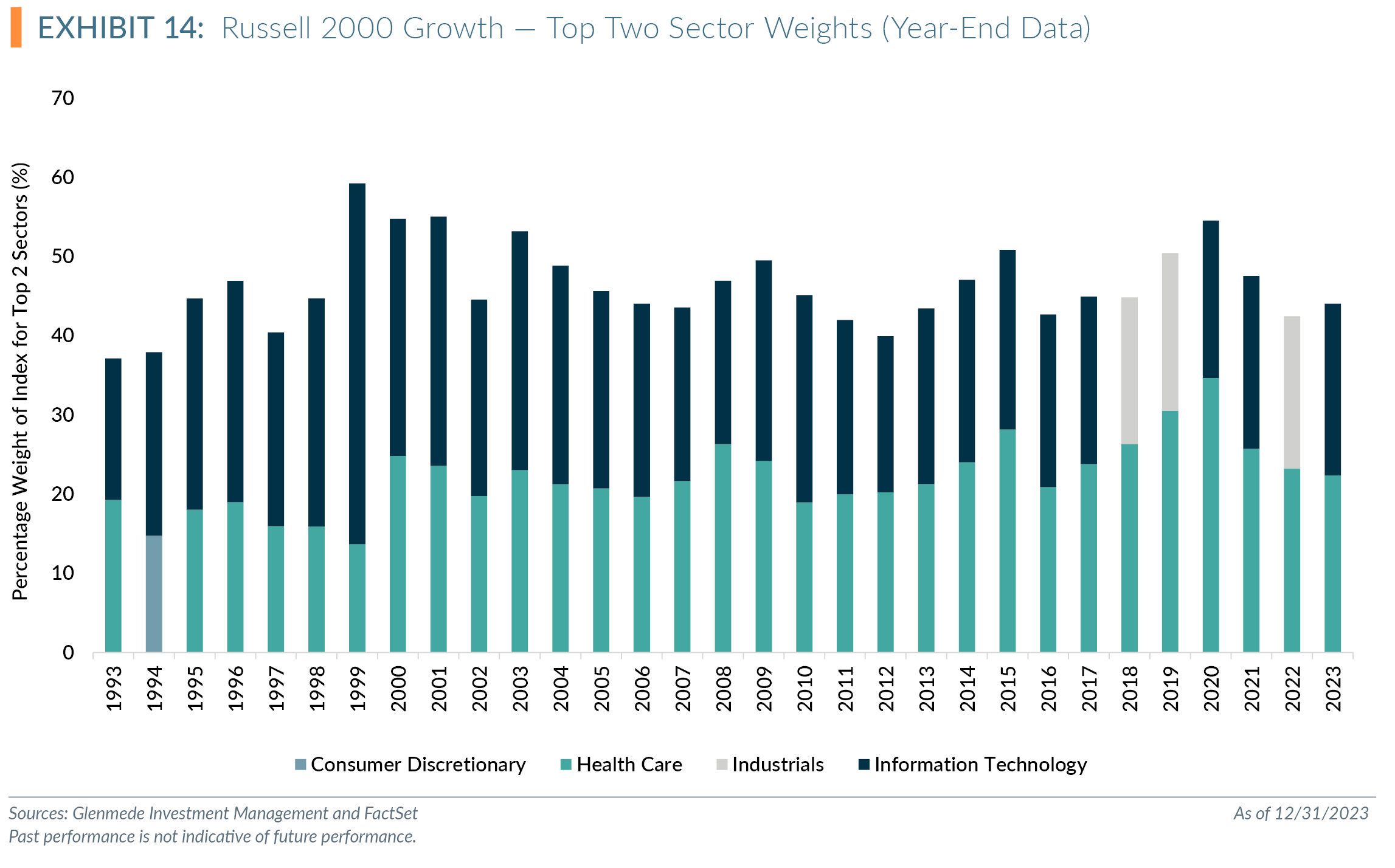

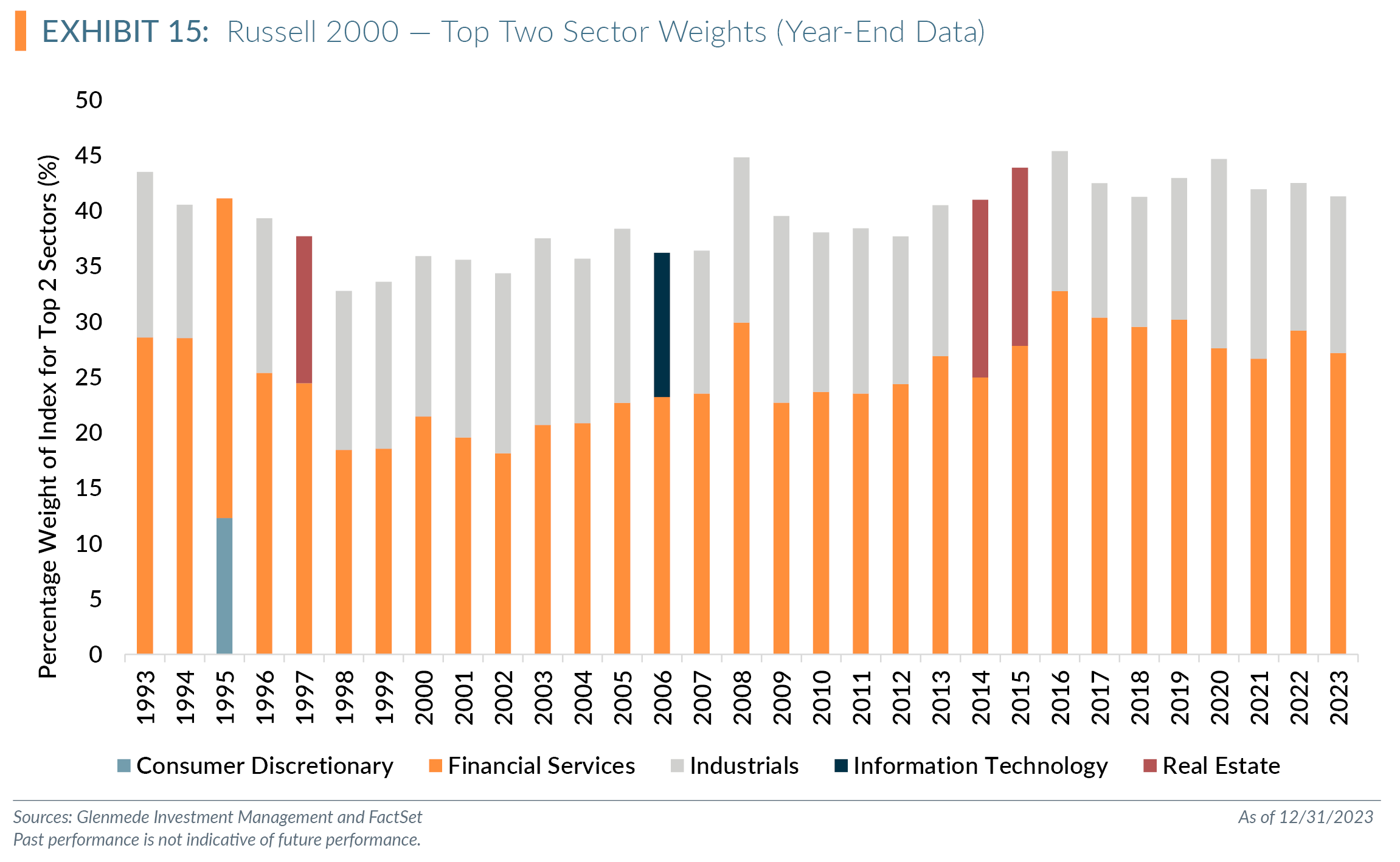

Sector exposure also becomes a risk with a style-specific strategy. As shown in Exhibits 13, 14 and 15, the concentration of sectors within the style indices could lead to less diversification than a core manager. Exhibits 13, 14 and 15 show the top two sector exposures for the Russell 2000, Russell 2000 Growth and Russell 2000 Value indices over the past 30 years using year-end data. The median weight of the two sectors for the Russell 2000, Russell 2000 Growth and Russell 2000 Value are 33.3%, 45.0% and 39.5%, respectively. Growth exposure has historically been heavily weighted to healthcare and technology, value exposure to financials and industrials and core more variation with financial services, technology and industrials rotating through the top exposures regularly. With varying flavors of aggressive, deep or relative style tilts, pairing style managers may lead to unintended over- and under-exposures. With a core strategy, allowing the freedom of exposure to the more attractive opportunities without style or sector restriction can lead to better risk-adjusted returns.

U.S. Small Cap: 2024 and Beyond

Assuming nothing has fundamentally changed, and the cyclicality of large-to-small performance remains, as shown in Exhibit 8, we believe small cap is poised to close the gap of underperformance relative to large cap in the coming years. More specifically, given the starting valuation levels of the positive earners in the Russell 2000 Index relative to the Russell 1000, as shown in Exhibit 10, we believe that positive earning small cap companies offer the more attractive risk/reward relative to the large cap counterparts and can potentially outperform in 2024 and beyond. We also continue to believe that exposure to an active small cap core strategy versus splitting an allocation or trying to tactically time a style tilt is a more reasonable approach.

2024 and More Thoughts

We believe the Fama-French size factor begins to normalize and strategies that overweight exposure to smaller, attractively valued companies will outperform strategies with concentration to the largest, more expensive companies.

1 Please see our Q2 2023 Quarterly Statement, “Concentration…64…No Repeats…Or Hesitation”, and May 2023 white paper, “Concentration Traps of Equity Indexing.”

2 The Fama/French Three-Factor Model is a statistical model developed by Eugene Fama and Kenneth French to describe stock returns using three factors: 1) overall market risk, 2) outperformance of small versus big companies and 3) outperformance of high versus low book-to-value companies. Data can be found at https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html

3 We define a negative earner as any company without earnings over the trailing 12 months. For additional reading on negative earners, please see Why Profitability Matters: Positive versus Negative Earners and Negative Earners Could Create Positive Alpha for Active Strategies.

All data is as of 12/31/2023 unless otherwise noted. Opinions represent those of Glenmede Investment Management LP (GIM) as of the date of this report and are for general informational purposes only. This document is intended for sophisticated, institutional investors only and is not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally. GIM’s opinions may change at any time without notice to you. Any opinions, expectations or projections expressed herein are based on information available at the time of publication and may change thereafter, and actual future developments or outcomes (including performance) may differ materially from any opinions, expectations or projections expressed herein due to various risks and uncertainties. Information obtained from third parties, including any source identified herein, is assumed to be reliable, but accuracy cannot be assured. This paper represents the view of its authors as of the date it was produced, and may change without notice. There can be no assurance that the same factors would result in the same decisions being made in the future. In addition, the views are not intended as a recommendation of any security, sector or product. Returns reported represent past performance and are not indicative of future results. All results reported are of unmanaged indices, used just as illustrations for various market segments. These do not reflect what an actual investment in this sector would achieve, as it includes no accounting for trading costs or fees. Performance of any particular investment in one of these market segments could be lower or higher than what is reflected above.